Florida panhandle beaches are some of the finest in the world. Pristine white powder. Pensacola is not the kind of place I wanted to visit for lessons about the fleeting nature of human existence, yet there I was. Life is full of cruel twists and turns. Throw the genetic dice often enough and someone you love (maybe even you) will roll snake eyes. It’s not fair.

Philistines are met by the Holy upon arrival in Pensacola. Bible-clasping gentlemen stand on four corners proferring salvation to drivers. Can a young man in a white shirt and black tie with perspiration rings forming under the sleeves reach a sinner with averted eyes at a red light? Does it ever work? Does anyone ever turn into the Dollar General parking lot to ask for directions to the on-ramp of righteous eternal existence? One is all it takes. One driver. One soul.

If you’ve read this far, you may be thinking, “Death and salvation? Is this guy always so serious?” The answer is “hell, no”. I just sat down to ponder the weighted average cost of capital and this is the weighty path I took. I offer no salvation, no divine guidance. I’m not even very good with Google maps. But I decided to stand on a corner for the first time in a long time. Pen in hand. It’s good for my soul.

Mortality can be a pretty good business if you’re a skilled actuary. Promise to hand someone a large pile of dollars in the distant future in exchange for small cash payments over many years. Find enough healthy mortals to make lots of small payments, and immense wealth can be generated by investing these premiums before you have to return the piles of cash. The life insurance industry is really just about winning at the game of death. Outlast your policy holders and beat the clock. There are no Luka Doncic three-pointers at the buzzer on the court of life insurance. That’s because there’s no buzzer. The best life insurance companies tick along perpetually with Swiss precision.

Mutual of Omaha has been very good at the business of reinvesting insurance policy premiums. I decided to take a look at their most recent public financial reports. The venerable institution had over $9.6 billion in cash and invested assets at year-end 2023, and nearly $4 billion of policy holder surplus. I wanted to look at their financials to see how they are paying for the largest development in Omaha: the $650 million skyscraper that will soon become the tallest building on the horizon. I learned a few things reading their report:

- Similar to most real estate developers, a big slug of leverage is invloved: At March 17, 2023, “the Company entered into a $550,000,000 senior unsecured credit agreement that is available for purposes of funding the new home office building.” In real estate terms, Mutual of Omaha is just like Bruce Dickinson – they put their pants on one leg at a time.

- The bond bear market has not been kind to the fixed income portfolio. The worst sell-off of bonds in a generation left Mutual of Omaha with over $526 million of gross unrealized capital losses.

- Mutual of Omaha has $214 million of short-term outstanding borrowings from the Federal Home Loan Bank. This represents a significant increase from the $40 million borrowed at the end of 2022.

I don’t know that many conclusions can be drawn from these observations. Personally, I would not have sunk 7% of my investable assets in a building that will likely be worth 20% less the day it opens. But Mutual of Omaha is a perpetual financial insitution, not a cyncial and balding middle-aged guy with a computer and a finite time horizon. They will hold the asset for longer than its depreciation schedule and it is an emphatic statement of corporate strength. In other words, $650 million is a fair price to pay for permantently establishing your image as a solid financial giant when such an image is essential to your brand. There’s a reason why Louis Vuitton sells bags in a palace on the Champs-Elysees instead of a Carrefour in Nanterre.

Second, the losses on the bond portfolio present no threat. Unrealized losses are actually much improved from 2022 when they amounted to over $690 million. Mutual of Omaha matches its investments to its policy obligations and they epitomize the definitition of “held-to-maturity”. There is no risk of an imminent loss of capital. There is a downside, however, in the form of opportunity cost. $500 milion could be earning 2-3% more per year. Instead, Mutual of Omaha has to let those underwater bonds mature. Because the only thing worse than unrealized losses are…realized losses. It’s just the sort of income you might wish you had available if you were to, say, pay for a new office building.

Finally, the Federal Home Loan Bank borrowing raises some concerns. The FHLB window was opened wide last spring when some banks ran into liquidity issues. Are there liquidity issues in the Mutual of Omaha portfolio? It seems unlikely, yet the $175 million increase didn’t suddenly materialize out of nowhere. Calls were made. Flesh was pressed. Deals were done. Frankly, I did not even know that insurance companies could borrow from the FHLB. This was news to me. Apparently $134 billion has been loaned to insurers, and the low cost of funds present a wonderful arbitrage opportunity. Imagine that. A taxpayer-backed hedge fund mechanism. I’m not sure how I feel about being the backstop for more leverage in the housing system. But as the saying goes, “Teach a man to arbitrage…”

So, there you have it. Dante might be proud. We started our little story with damnation and ended with a cursory look at the financial results of an insurance company specializing in death benefits. As a wise man once sang, “Don’t fear the reaper.”

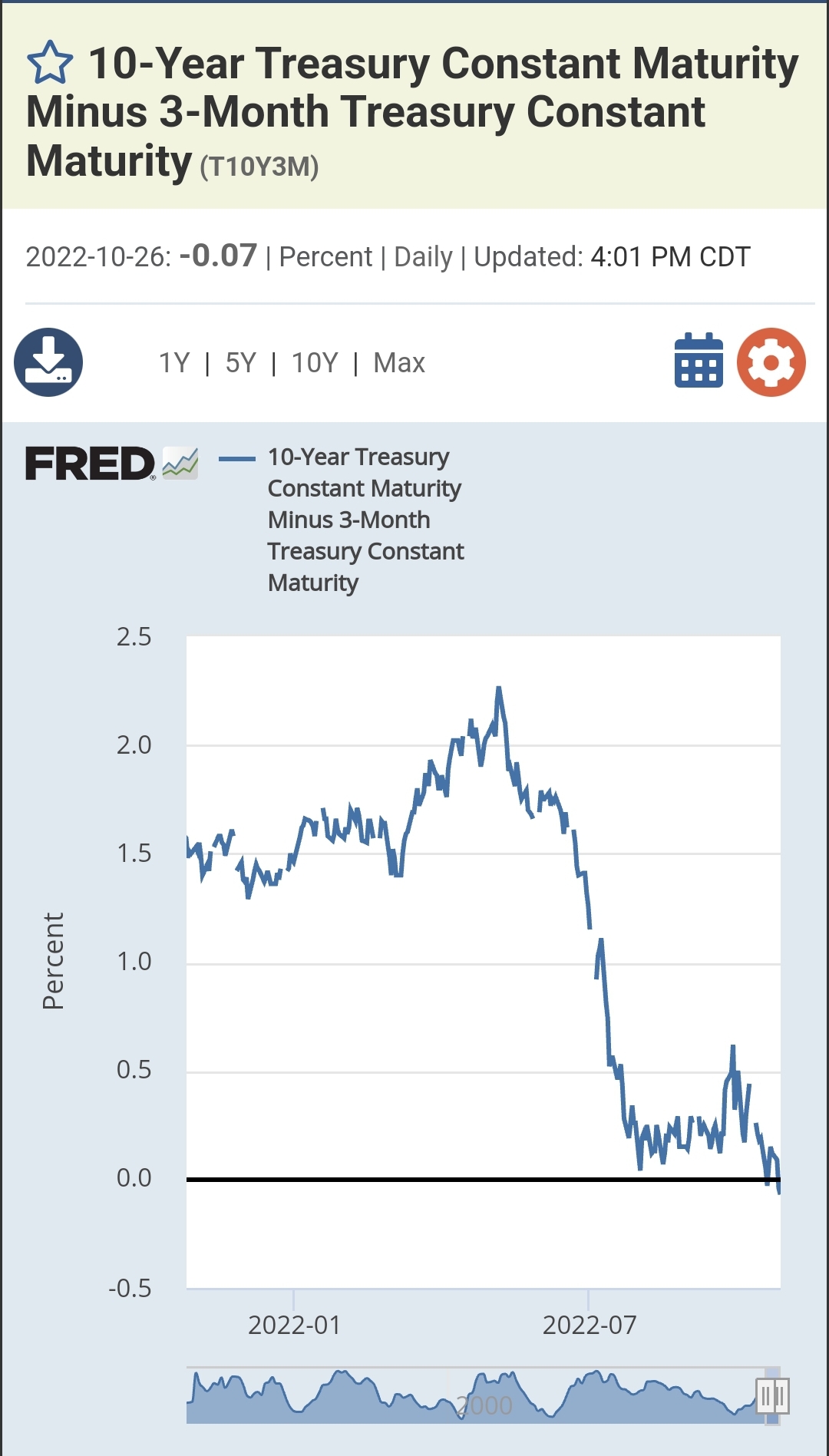

For a moment today, the three-month United States Treasury Bill offered a yield higher than what could be earned by loaning the government money for ten years. Prepare accordingly.

Congratualtions to Barb! She is leaving Alchemy Development and joining a leading engineering firm in Omaha. Barb joined Robert Hancock & Co. in 2004 and went on to manage construction projects including Pinhook Flats, Cue and Shadow Lake Square. She has been an outstanding partner and her experience and wisdom will surely be missed. We wish her all the best on her new journey.