A Substack went viral the other day talking about how a minority of published posts on the platform generate the majority of views. When no part of earth shattered at this revelation, the author pressed the argument by citing something called Price’s Law. Since it had an equation with a square root in it, the whole concept seemed pretty legit.

To my eyes, it looked like a more sophisticated version of Pareto’s 80-20 observation. Regardless of which polymath you prefer, it drew the same conclusion – a few of your most successful ideas generate most of your income. The piece seemed to argue in favor of “flooding the zone” with material, since it couldn’t be known with any confidence what was going to catch fire. At least not until one applied rigorous scientific observation once sufficient data had been assembled. This reminded me of Ken Griffin’s remarks about needing to be right only slightly more than 50% of the time. Or was that Roger Federer?

Of course, this all assumes that any of us are capable of heroic levels of output. There are only so many Danielle Steels in the world. Nor do most of us have a team of geniuses generating such creations on our behalf. I can only hope I will live long enough to see the day when Silicon Valley invents a computerized program that can simulate human intelligence. Until then, it’s just me.

I suppose the counterargument would come from Grandpa B about only having 20 punch cards in your life, or something to that effect. There’s also his admonition to avoid the institutional imperative that comes to mind. Producing more content because everyone else is producing more content is how you end up with slop. Does Irenic really need to start an activist campaign to revitalize Snap? It’s also how you end up with the military-industrial complex that Eisenhower warned us about. But that’s a different newsletter.

All of this is a long way of saying: 1. It’s been awhile since I wrote anything. 2. That doesn’t mean I haven’t had any ideas lately. It just means I haven’t had the time to “craft” anything worthy of production. 3. Should that even matter? Perfection is not my goal. This is simply a forum for me to think out loud. And if a few people read it and give me constructive feedback, well then, I’m learning. If someone makes some money out of these observations, then that’s good too. 4. Perfection is not much fun anyway. We’re not writing the last page of Farewell to Arms for 47 iterations to find the answer. I have really enjoyed Eden Bradfield’s writing. There’s a grammar error here and there, but it’s real stuff. The rough edges are part of the charm.

So, enough of the beard-stroking. Here are a couple of REITs I’ve been thinking about. The first one is BRT Apartments Corp. $BRT, and the second is Americold Realty Trust $COLD. I’ve taken a sizable position in BRT but remain on the sidelines for COLD. Yes, the sentiment for refrigerated warehouse space is especially bearish. The Wall Street Journal recently talked about the oversupply in the sector and the concomitant consumer spending slowdown.

I know a little about refrigerated warehouses from experiences early in my career and I can tell you a couple things. One, you are running a service business where tenants have high inventory turns. It’s more like a hotel than a warehouse. Two, it’s a hell of a lot more seasonal than you might think. It seems totally obvious, but most turkey gets consumed in November and December. Most of those birds are sold frozen. No matter how good your logistics are, it’s just not possible to kill millions of turkeys in October, freeze them, and then ship them in November. No, it’s a cyclical inventory build over several months. Kind of like Mattel placing orders for Barbie in July. It takes time to amass a lot of turkeys. And then whoosh. Out they fly, er, out they ship. I’m sure most of the high-end steak business has a similar cycle.

The point here is that you may think you can just evaluate a refrigerated warehouse portfolio as real estate, but you really need to factor in lot of management. Probably much more than you’d have in a net-lease industrial realty business. Let’s take Prologis, the biggest industrial landlord. In 2025, Prologis had general and administrative expenses of $469 million on $8.8 billion of revenue, or just about 5.34%. In contrast, Americold has $269 million of G & A expenses on $2.6 billion revenue. That’s almost double.

Why is this important?

Well, a lot of people use the exercise of applying a capitalization rate on net operating income (NOI) to arrive at value the underlying assets. NOI is a real estate cousin to EBITDA, and most REITs publish this number for us real estate hillbillies followers to consider. When they compute NOI, they add back general and administrative expenses. The theory here is that a buyer of the individual properties wouldn’t be burdened by the parent company’s management costs.

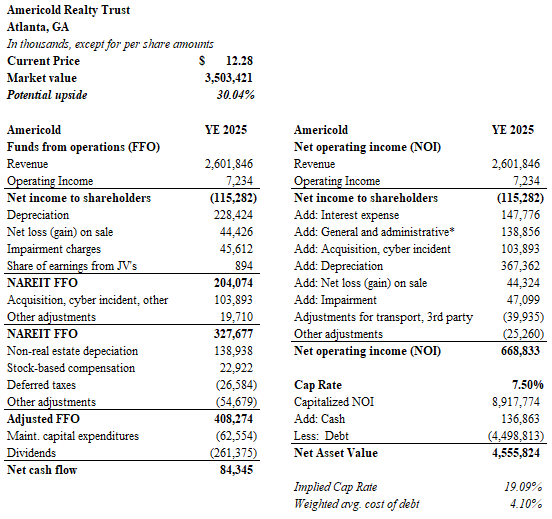

The casual observer might take the NOI for Americold at the end of 2025 and make the assumption that the assets are worth $13.3 billion. COLD published NOI of $800 million at the end of 2025, so $13.3 billion is what you get with a 6% cap rate. Let’s use 6%, since that’s about 200 basis points above the company’s current debt cost. Subtract debt of $4.5 billion and the net asset value could be $9 billion. The market cap for Americold is only $3.5 billion. Before you run to your Robinhood account, take a breath. Unfortunately, these assumptions are far too aggressive. Adding back $269 million of general and administrative expenses is not realistic. These are businesses as much as they are buildings, and sweeping aside a layer of management is simply not possible.

I decided to value the real estate using a 7.5% cap rate. Investors in institutional quality real estate would probably argue in favor of a lower rate, but I figure the current cost to borrow money is more like 5.5% and I’d still want to earn 200 basis points over that number. It’s also a soft market. As a general practice, I don’t think you should underwrite deals by penalizing them with the bigger cap rate. Rather, you should make the adjustments in your future rent assumptions. You may want to assume that revenues will fall by 10% for refrigerated warehouses given the oversupplied market conditions. Such a rent reduction would knock $260 million off the top line, and eviscerate $3.5 billion of value. Maybe the market knows this, and that’s why the chart for COLD looks worse than the Thwaites Glacier.

I don’t have time for a rent sensitivity analysis, nor do I know the market that well, so I will just use 7.5% as my cap rate in this exercise. Hypocrisy be damned.

Instead of adding back $269 million dollars of general administrative expenses, I added back $139 million. This number represents 5.34% of revenues, just like at Prologis. In other words, I’m saying $130 million of general and administrative expenses are an integral part of Americold’s business and can’t be removed for purposes of valuing the real estate. The resulting NOI is $669 million. Let’s capitalize that number at my 7.5% to arrive at an asset value of $8.9 billion. Less debt, the net asset value for Americold calculates to $4.5 billion. This is approximately 30% above COLD’s market capitalization. The market offers a decent discount, and it explains why Ancora Holdings has agitated for changes, including asset sales.

The 7% dividend yield is attractive and seems reasonably well covered if you believe management’s figures that maintenance capital expenditures amount to $62.5 million per year. This strikes me as a little on the low side, but I am just asking the question. I don’t have comparable data. I will say that refrigerated warehouses are filled with complicated cooling systems that require a lot of maintenance. Underestimate that number at your peril.

My verdict here is that a Americold presents a good value. The dividend seems like a solid way to earn some beefy yields while Ancora puts the company’s assets through their paces. Leverage is about 50% of my estimated value, so that’s a little high. One could envision a dividend cut if funds need to be marshalled for principal reductions. Fortunately, the company’s debt maturity timeline is long. The oversupply in the market will eventually be absorbed. I set Americold on the back burner for now, but I will likely revisit the business soon.

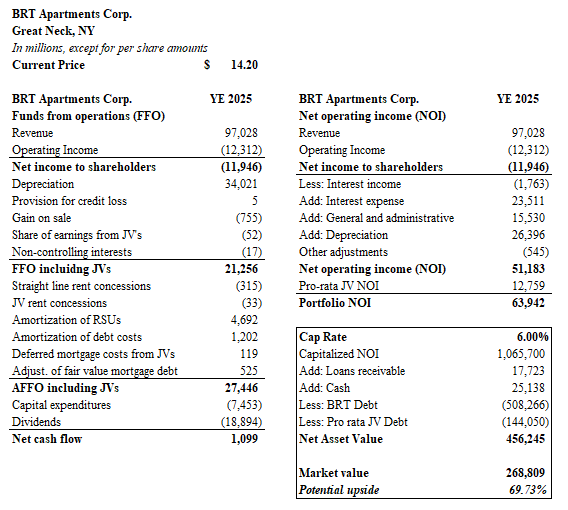

I have much more confidence in BRT Apartments Corp. The company is based in New York and owns about 5,400 units throughout the southeast. Many properties are held through joint ventures. The company is controlled by the Gould family. I have read various estimates about the amount of insider ownership at BRT, and it seems like it is nearly 95% when I toted up the 13-Fs. So, there’s not much float. No activists are going to come along and move the needle. The Goulds probably aren’t in a hurry to make any aggressive changes. The company’s dividend reinvestment program works in their favor. There’s no identifiable catalyst, in value investor parlance.

Despite these caveats, BRT is an exceptionally cheap stock. I owe a hat-tip to an Omaha fund manager. I would name him but I won’t, since I suspect he would like to add to his own position under the radar. The thin trading volume has meant that recent purchases have already pushed the share price above $14. It was $13.50 when I made my initial buys. The current market capitalization is $269 million, but I think the net asset value exceeds $456 million. BRT pays a 7% dividend yield – far higher than Avalon Bay $AVB and Mid-America $MAA. The assets are solid B+/A- apartment communities in dynamic metro areas. Yes, some of those markets have been fairly soft and the share discount may reflect some concerns about looming vacancy issues. The portfolio is also 60% leveraged, so there’s a riskier element to the business than some of the bigger multifamily REITs.

I’m not going to write a lot more here since I’ve already overstayed my welcome, but I will say that it is very hard to justify digging a hole for a new apartment complex right now when an investment like BRT is available as a public entity. One would be hard-pressed to generate a 7% cash-on-cash return today on most new developments using an equivalent percentage of leverage. With tons of money still out there chasing deals, the yield on most acquisitions would be even lower. BRT is certainly very attractive when compared to private market alternatives.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

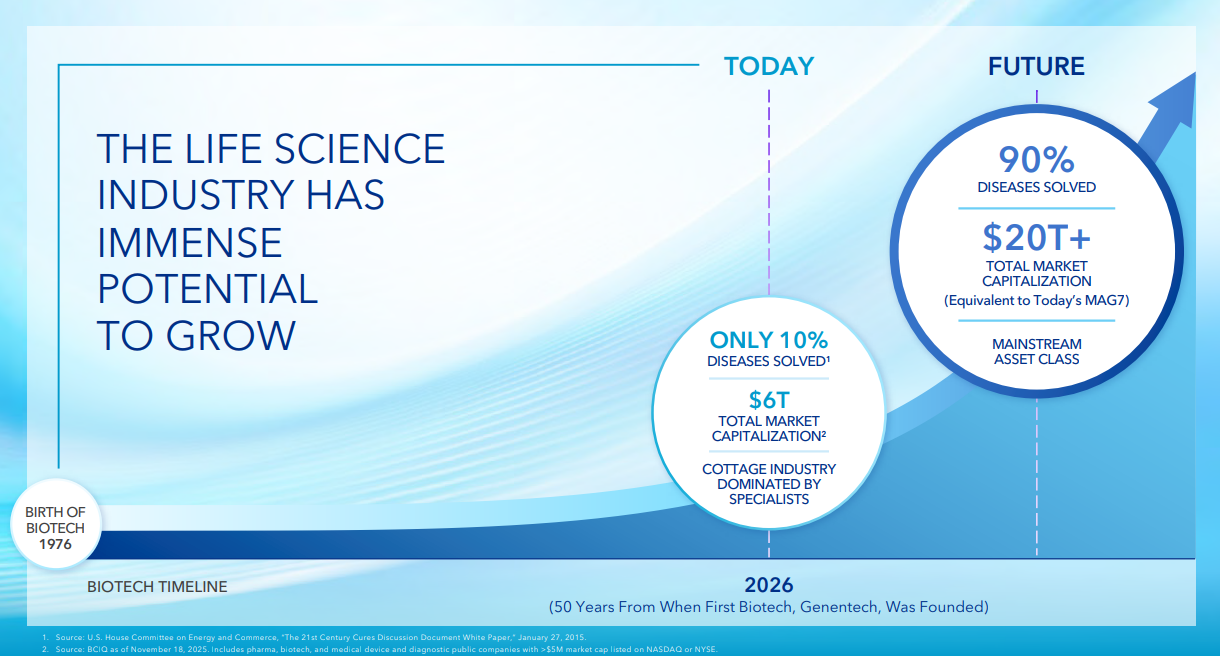

I don’t know if they hand out awards for the most optimistic investor relations team, but the gang at Alexandria Real Estate Equities just opened 2026 with a banger that will surely make them the top candidate. Yes, it’s been a rough three years for the nation’s largest owner of buildings dedicated to the pharmaceutical and biotechnology industries. The share price has fallen by 75% since the pandemic and they just slashed the dividend. But despair not ye of little faith. Just think about all of those diseases out there looking for a cure!

The Alexandria slide deck announces our glorious pharmaceutical future by declaring that only 10% of earthly diseases have been “solved”. That leaves 90% of the rest of the diseases left to cure. Talk about upside! The current market capitalization of the biotechnology industry is estimated by Alexandria to be $6 trillion. Extrapolating this figure for the next 80%, well, that’s another $14 trillion of potential market capitalization lying just beyond the rainbow. The god-like powers of capitalism will save humanity.

Alexandria’s team must have considered the irony of this future. After all, once 100% of the remaining diseases are “solved”, the market capitalization of the biotech industry should be closer to zero than $20 trillion. Realizing the potentially adverse effect of curing all diseases, they left open the possibility that 10% of the remaining diseases are beyond the grasp of even the most miraculous biotechnical engineering.

Because, when you get right down to it, solving all diseases isn’t great for business. No, what we really need is a sort of Munchausen-by-proxy economy. By all means, come up with ways to treat the ills of mankind which improve comfort and extend lifetimes. But cure? Now, hold on there, that’s a lot of jobs we’re talking about. Healthcare is now more than 16% of our nation’s GDP. You know what might work even better? What if we re-introduced diseases that were already “solved”? Take measles, for instance. Who knows? A resurgence of leprosy might be just what we need to avoid the next recession.

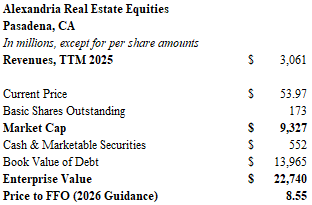

Ok, enough joking around. In fairness to Alexandria, much of the presentation describes the precarious state of the life sciences real estate market and the challenges facing the company. The real question before the house is whether shares in Alexandria Real Estate Equities (ARE) offer investors compelling value. The nation’s largest owner of real estate dedicated to scientific research claims that the net value of its assets is far higher than the current $54 share price. Alexandria’s investor presentation asserts that the true value is closer to $94. In my estimation, the shares are worth about $73. However, I won’t be buying stock any time soon. Much of this premium is based upon the book value of an uncertain development pipleine and the value of its speculative securities investment portfolio.

In this article, we’ll take a brief overview of the latest investor presentation, and I will guide you through some numbers that compose my valuation.

Alexandria has shaped its nationwide real estate portfolio into 26 dynamic innovation campuses. Primary markets include Boston, San Diego, San Francisco, Seattle, and DC. The company boasts a tenant roster of 700 companies in 27.1 million rentable square feet. Tenant retention has been over 80% over the past five years. Scientific innovation thrives when disparate groups of creative thinkers interact on a frequent basis. Despite the rise of remote work, it seems likely that medical technology will continue to emerge from the laboratories and offices of pharmaceutical companies, research universities, and medical device manufacturers.

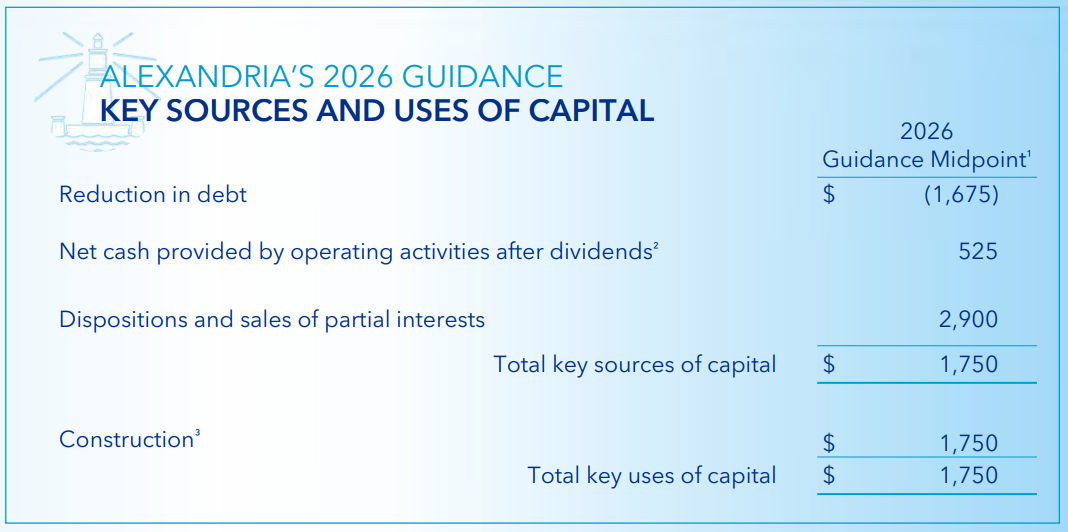

Alexandria trades with a market capitalization of $9.3 billion and the current price allows for a 5.3% dividend yield on the reduced payout. The share price is roughly 8.6 times management’s guide for 2026 funds from operations (FFO). The undepreciated book value of real estate on its ledger amounts to $29.3 billion, with another $8.6 billion of construction in progress at the end of the 3rd quarter of 2025. The company has approximately $13.9 billion of debt and lease obligations. To improve the balance sheet, Alexandria intends to dispose $2.9 billion of “non-core” real estate assets and joint venture interests in 2026. ARE forecasts 2026 operating cash flow (after dividends) of $525 million. The resulting $3.4 billion cash pile will be split: $1.7 billion for debt reduction and $1.7 billion for the completion of construction projects.

Alexandria is rated BBB+ by Standard and Poor’s but has been placed on a negative credit watch. Still, the company does benefit from a low cost of financing and a long runway for debt maturities. The weighted average interest rate for ARE’s debt is 3.97% and the weighted average maturity is 11.7 years. Unfortunately, recently issued debt came with a 5.6% coupon.

The reasons for worrying about Alexandria’s future are easy to find. Winter has arrived for the medical technology industry. Demand for life science space has fallen 60% since the pandemic. To make matters worse, the most recent Senate budget presents a 40% decline in spending for the National Institutes of Health (NIH) to $48.7 billion. It is estimated that 1,500 jobs will be eliminated. Meanwhile, only about $9 billion of venture capital funding is anticipated for the medical technology industry in 2026. This represents a substantial reduction from 2021 when $41 billion was raised. Pharmaceutical company spending on research and development peaked in 2023 at $317 billion and has fallen the past two years.

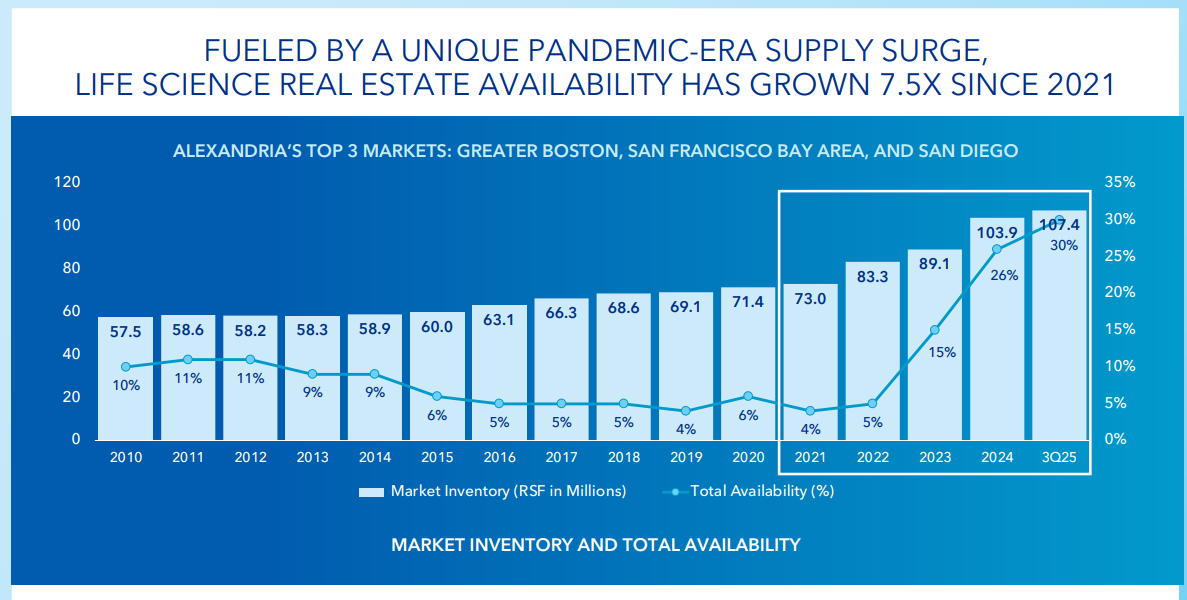

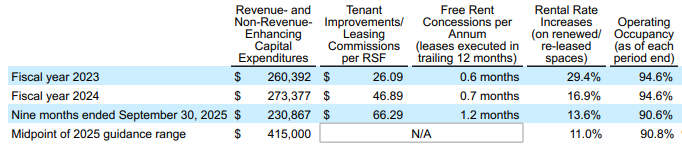

Market occupancy levels have dropped precipitously. Over 30% of space is available in the company’s top three markets of Greater Boston, the San Francisco Bay Area, and San Diego. Occupancy levels at Alexandria’s buildings reflect the industry decline. They fell dramatically from 94.6% at the end of 2024 to 90.6% at the end of the 3rd quarter of 2025. Any time real estate owners see an occupancy level with an 8 in front of it, beads of sweat start to appear. Occupancy at Alexandria is forecast to drop to as low as 87.7% by the end of 2026.

More problems could lie ahead. Alexandria has a plan for 2026, but what about the completion of projects in 2027 and 2028? Future capital raises to finish buildings in progress may be needed, and they will certainly dilute current shareholders. At the end of the 3rd quarter of 2025, Alexandria projected that 4.2 million rentable square feet will be placed into service between the end of 2025 and 2028. 43% of the new space is under lease or in negotiation. This new space is expected to generate more than $390 million of NOI. But that assumes another 2 million square feet has yet to be absorbed in what promises to be a soft market. It could take many years to backfill the overall 30% market availability in Cambridge, Massachusetts.

Finally, the entire cost structure of newer assets may face a pricing reset. Capital improvements amounted to $260 million in 2023, but they were expected to rise to $415 million by the end of last year. On a per square foot basis, TI’s and commissions rose from $26 to $66 over three years. Free rent to secure new leases has doubled during the timeframe. Even the strongest pharmaceutical companies will balk at the rental rates on offer and demand substantial concessions.

Alexandria forecasts that 2026 FFO will fall from approximately $9 per share in 2025 to $6.40 per share in 2026. While dispositions account for a large portion of the reduction, rents on lease renewals are forecast to fall by as much as 12%. Same-store net operating income will drop by as much as 9% in 2026.

Valuation

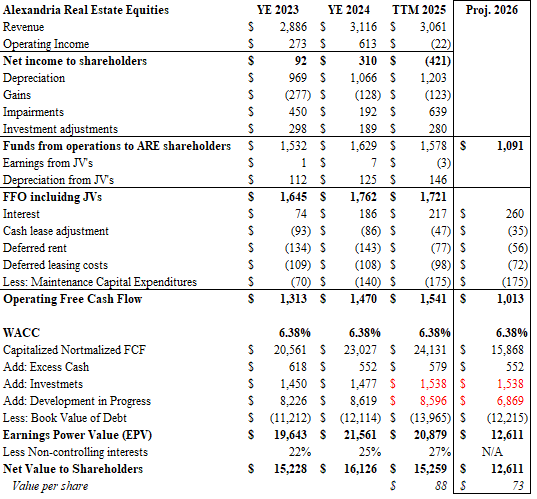

My valuation method is very simple. I took $1.1 billion of projected funds from operations for 2026, added back the forecast interest expense of $260 million, subtracted $175 million for maintenance capital expenditures, and subtracted cash lease adjustments. The cash lease adjustments are identical to the numbers for 2025, but they have been reduced by 27% to estimate the portion attributable to joint ventures. The resulting free cash flow from operations for 2026 is estimated to be approximately $1 billion. This sum was divided by a capitalization rate of 6.38% to arrive at $15.9 billion of value.

Next, I added $552 million of cash on hand, the securities investment portfolio of $1.5 billion and the book value of construction in progress of $6.9 billion. Construction in progress was calculated by subtracting $1.75 billion from the September 2025 balance of $8.6 billion. Finally, after accounting for management’s guidance of $1.75 billion of debt reduction, the 2026 debt level of $12.2 billion was subtracted. The net value is $12.6 billion, or approximately $73 per share.

The table shows the change in computed net asset value over the past three years. In 2023 through 2025, I “grossed up” funds from operations to include joint venture partnerships before capitalizing the cash flow. An adjustment was made at the bottom using a percentage of book value attributable to noncontrolling interests. My calculation for 2025 indicates a net asset value of $88 per share, showing that a substantial decline in the stock was justified.

My capitalization rate is based on a weighted cost of capital where the market value of net debt accounts for 56% of the measure. At a BBB+ rating, the cost of debt was attributed as 5.1%. This is a forgiving number considering the recent placements at higher rates. Equity, the remaining 44% of the weight, was awarded a simple 8% rate. I don’t have a sophisticated explanation for the use of 8%, but it generally “feels right”.

You may think my cap rate is too high considering the gold-plated roster of tenants like Lilly and Merck and the proximity to the best universities in the world. Alexandria touts its asset values utilizing capitalization around 6% and below. Yet, the company has sold assets at cap rates above 8.5%. The building sales may may not represent “core assets,” but such a wide discrepancy can’t persist as long as interest rates remain elevated.

Although the calculation offers the appearance of upside, far too much weight is placed on the book value of construction in progress and the value of the company’s securities. Alexandria often took equity stakes in their tenants in lieu of rent. Given the uncertainty around new drug approvals, much of the securities portfolio could become impaired. Meanwhile the full lease absorption of $6.8 billion of construction in progress is far from certain. In the early years following completion, hefty concessions will be required to attract tenants. One can easily see that a 30% impairment of the development pipeline would eliminate the premium calculated in my valuation. The market may well be ascribing such a discount already.

Alexandria Real Estate Equities offers an intriguing way to invest in the future of the pharmaceutical industry. Medical innovations will continue to emerge, of course, and they may occur more frequently than not at one of Alexandria’s campuses. The company has a best-in-class real estate portfolio and has proven to be a skilled operator and attractor of premier tenants. But nobody is immune to the laws of supply and demand. There is simply too much laboratory space on the market, and the engines of demand are looking fairly dormant. When the government is no longer a key partner in the development of new drugs, your runway looks a lot cloudier. Is there upside? Probably so. But, I think there are better places to put your money in the meantime.

If you are attracted to Alexandria’s robust dividend yield, I would look elsewhere. Some of the pipeline master limited partnerships (MLPs) are more appealing. Western Midstream (WES) and Hess Midstream (HESM) yield about 9%, and the demand for natural gas seems much more reliable as power generation capacity continues to grow. Along those same lines, some of the big miners stand to benefit from the copper and minerals boom. BHP yields 3.5%, Rio Tinto is on 4.6%, and the much riskier Vale yields more than 8%. I would add that the large mining companies provide the added benefit of diversifying away from a deflating dollar.

We’ll leave it there for now. Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

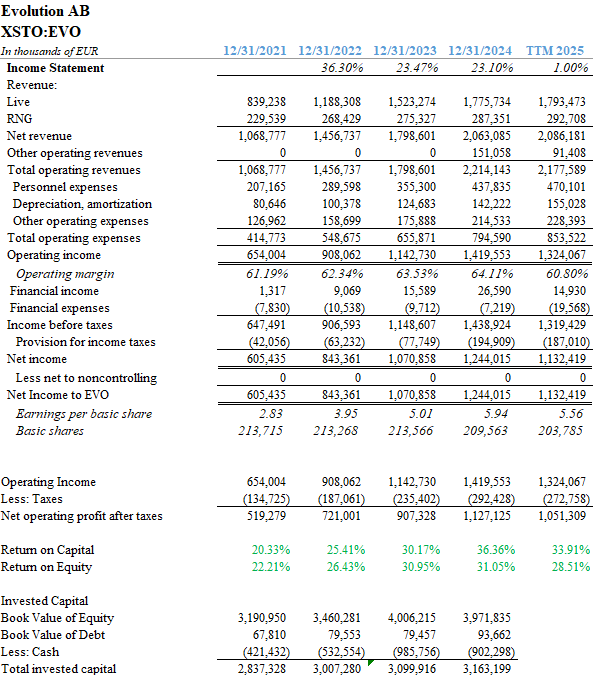

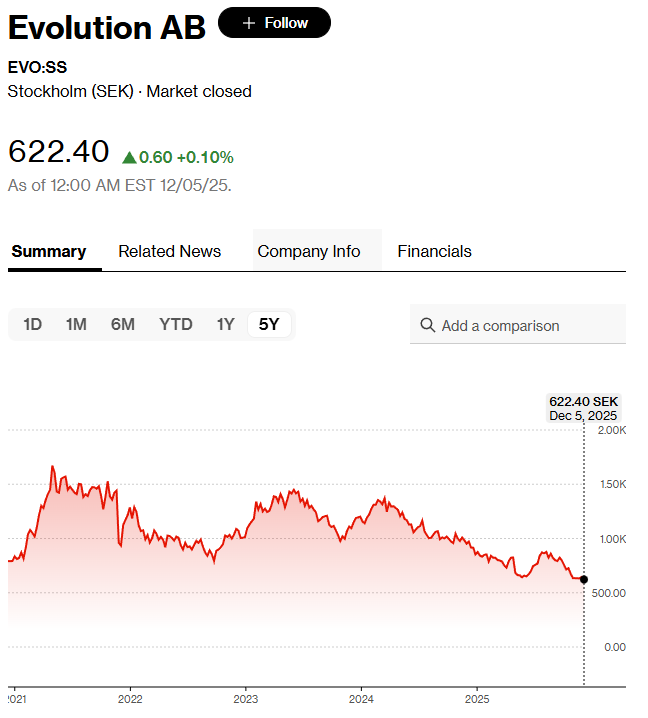

Evolution AB is a Swedish gaming company that trades on the Stockholm bourse. About 622 krona will buy you a share, and that price gives Evolution a market capitalization of about €11.6 billion. Evolution develops and operates games that “sit behind” many well-known gambling sites. They continually find new dopamine-enhancing ways to keep punters glued to their devices, losing money to the house in rapid-fire succession. Most games seem to target the unsophisticated bettor. “Coin Flip”, “Cash Hunt” and “Crazy Time” are just a few of the offerings. More interestingly, they also offer traditional casino games like poker and roulette by hosting players online with live studios situated around the world.

I passed on Evolution earlier this year, but I decided to take another look at after reading a recent Bloomberg article about the investment activities of Kenneth Dart who is taking large positions in the gambling industry through Evolution and Flutter. Flutter owns FanDuel, Paddy Power Betfair, SportsBet, and Poker Stars. Or, if you prefer, just about half of the kit sponsors for English football. In a clear indication of modern society’s moral compunctions, England has banned alcohol sponsors on their team jerseys for well over a decade, but they have no problem with gambling companies emblazoned across players’ chests.

Kenneth Dart is the billionaire heir to the plastic container fortune. When he’s not crafting ways to avoid paying taxes, he is busy investing in “sin stocks”. He had a phenomenal run of success with tobacco firms recently. The thesis seems to be similar for his investments in online gambling: it’s widespread, increasingly legal, and totally addictive.

Evolution trades with a trailing PE slightly above 10, and an EV/EBITDA multiple of 7.4x. After a brief summer rally, shares hover near 52-week lows. Evolution is 62% below its all-time Covid high, and down 26% since the beginning of 2025. Notably, Dart’s largest investment in the company occurred before the most recent drawdown.

Revenues at Evolution grew at a compound rate of over 25% annually between 2021 and 2024. Unfortunately, the combination of high growth and diverse worldwide internet hosting services attracted the sort of nefarious folks who’ve always lurked in the gambling shadows. Hackers in Asia inflicted widespread outages and security breaches upon Evolution last year. Revenue has plateaued over the past 12 months. The stock price reflects the lost momentum.

Evolution’s leaders assure shareholders that the security problems have been solved and the company is ready to grow once again. I have found CEO Martin Carlesund’s messages to shareholders to be refreshingly blunt in their assessment of the company’s shortcomings. Accountability seems to be part of the vernacular at Evolution. It is a sharp contrast with another downtrodden company I have been researching: DentsplySirona (XRAY).

One might think that straight talk would be needed at a company which has lost 83% of its market capitalization, but that is not the case! DentsplySirona is not only a really horrible name (did they leave out letters to remind us of missing teeth?), the annual report is a load of jargon-filled blather that leaves one wondering if the company is a dental supply company or a multi-level marketing scheme. It certainly makes no apologies for an atrocious capital allocation track record and probably isn’t worth my time putting pen to paper. But we’ll talk about that later. Moving on.

Evolution is asset-light, has an operating margin of 60%, and posts returns on capital in excess of 30%. The company pays a well-covered dividend, and the yield is nearly 5%. If they can right the ship and return to growth, the upside is compelling.

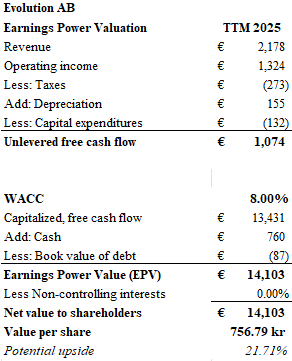

My preferred valuation model is the basic Earnings Power Value (EPV) method advocated by Bruce Greenwald and his peers at Columbia. In the tradition of Ben Graham, normalized unlevered free cash flow is simply capitalized by the weighted average cost of capital (WACC) to arrive at a value for the firm. Subsequently, net debt is subtracted to arrive at a value of the equity. In the case of Evolution, unlevered free cash flow over the trailing twelve-month period was just slightly less than €1.1 billion. Using a WACC of 8% to capitalize this amount results in a value of €14.1 billion once one accounts for the net cash position on the balance sheet. On this basis, Evolution trades at a 22% discount to its market price.

As always, I struggle with the proper cost of equity to employ in my valuation. I don’t use betas and assigning a cost to the equity is easier if you can assume a spread above the firm’s cost of debt. Since Evolution is unlevered, the 8% rate has a swaggy feel to it. Should it be lower? This is not a European company. Revenues are international, so pricing off the 10-year Bund doesn’t work. Arguably any company that is vulnerable to hacking and relies on programming talent anywhere from Tbilisi to Taipei should be valued accordingly. Using a WACC of 10% puts the value closer to par.

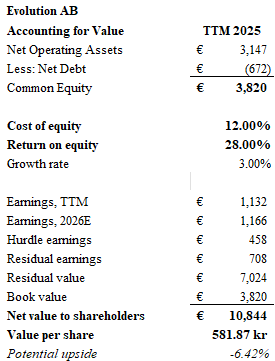

The other valuation model I’ve been using lately is the “accounting for value” method from the book Financial Statement Analysis for Value Investing. Stephen Penman and Peter Pope are CPAs by training and they take book value as the foundation. Next, they add the value of future growth. The authors rightly state that a company’s future growth is only valuable to the extent that the return on equity exceeds the cost of equity. They take this “surplus” return and discount it at the cost of equity less the assumed rate of growth. The higher the growth, the lower the denominator, the larger the value of future earnings. The model can be especially useful if one works backward: it tells you what level of growth is necessary to justify the current price.

If one assumes a cost of equity of 12% for Evolution, and a return on equity of 28% consistent with recent performance, the future “surplus” earnings calculate to €708 million assuming a growth rate of 3%. This results in a value 581 krona per share, once again, roughly in line with the current price.

But what happens if growth resumes at a rate higher than 3%? A 5% future growth rate results in a share value of $705 krona, or 13.4% upside. A 6% growth rate translates into $798 krona, or 28% upside.

Is the market for online gambling going to grow faster than worldwide GDP over the coming decade? It seems plausible. There is an insatiable willingness to gamble on literally everything, and the ubiquitous access to gaming through a phone makes it easily accessible. Might there be a backlash? Names like “Coin Flip” and “Cash Grab” imply a simplicity that can be very appealing to children, so it wouldn’t be surprising if there is a worldwide recognition that the proliferation of gaming is leading to problems with youth delinquency. But sadly, I think that regulatory horse has left the barn.

Evolution has created a lot of valuable intellectual property, its games are entrenched in the gambling site ecosystem, and the investment in live studios provides punters with the authentic feel of a casino. The lack of debt, high dividend yield and substantial margins seem to present downside protection. I believe the returns on equity are significant enough that the firm can reinvest its ample cashflow into growth that will exceed 5% over the next decade, so I consider the shares of Evolution to be priced 10-25% below the intrinsic value of the business. Fortis fortuna adiuvat.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.