Pareto

A Substack went viral the other day talking about how a minority of published posts on the platform generate the majority of views. When no part of earth shattered at this revelation, the author pressed the argument by citing something called Price’s Law. Since it had an equation with a square root in it, the whole concept seemed pretty legit.

To my eyes, it looked like a more sophisticated version of Pareto’s 80-20 observation. Regardless of which polymath you prefer, it drew the same conclusion – a few of your most successful ideas generate most of your income. The piece seemed to argue in favor of “flooding the zone” with material, since it couldn’t be known with any confidence what was going to catch fire. At least not until one applied rigorous scientific observation once sufficient data had been assembled. This reminded me of Ken Griffin’s remarks about needing to be right only slightly more than 50% of the time. Or was that Roger Federer?

Of course, this all assumes that any of us are capable of heroic levels of output. There are only so many Danielle Steels in the world. Nor do most of us have a team of geniuses generating such creations on our behalf. I can only hope I will live long enough to see the day when Silicon Valley invents a computerized program that can simulate human intelligence. Until then, it’s just me.

I suppose the counterargument would come from Grandpa B about only having 20 punch cards in your life, or something to that effect. There’s also his admonition to avoid the institutional imperative that comes to mind. Producing more content because everyone else is producing more content is how you end up with slop. Does Irenic really need to start an activist campaign to revitalize Snap? It’s also how you end up with the military-industrial complex that Eisenhower warned us about. But that’s a different newsletter.

All of this is a long way of saying: 1. It’s been awhile since I wrote anything. 2. That doesn’t mean I haven’t had any ideas lately. It just means I haven’t had the time to “craft” anything worthy of production. 3. Should that even matter? Perfection is not my goal. This is simply a forum for me to think out loud. And if a few people read it and give me constructive feedback, well then, I’m learning. If someone makes some money out of these observations, then that’s good too. 4. Perfection is not much fun anyway. We’re not writing the last page of Farewell to Arms for 47 iterations to find the answer. I have really enjoyed Eden Bradfield’s writing. There’s a grammar error here and there, but it’s real stuff. The rough edges are part of the charm.

So, enough of the beard-stroking. Here are a couple of REITs I’ve been thinking about. The first one is BRT Apartments Corp. $BRT, and the second is Americold Realty Trust $COLD. I’ve taken a sizable position in BRT but remain on the sidelines for COLD. Yes, the sentiment for refrigerated warehouse space is especially bearish. The Wall Street Journal recently talked about the oversupply in the sector and the concomitant consumer spending slowdown.

I know a little about refrigerated warehouses from experiences early in my career and I can tell you a couple things. One, you are running a service business where tenants have high inventory turns. It’s more like a hotel than a warehouse. Two, it’s a hell of a lot more seasonal than you might think. It seems totally obvious, but most turkey gets consumed in November and December. Most of those birds are sold frozen. No matter how good your logistics are, it’s just not possible to kill millions of turkeys in October, freeze them, and then ship them in November. No, it’s a cyclical inventory build over several months. Kind of like Mattel placing orders for Barbie in July. It takes time to amass a lot of turkeys. And then whoosh. Out they fly, er, out they ship. I’m sure most of the high-end steak business has a similar cycle.

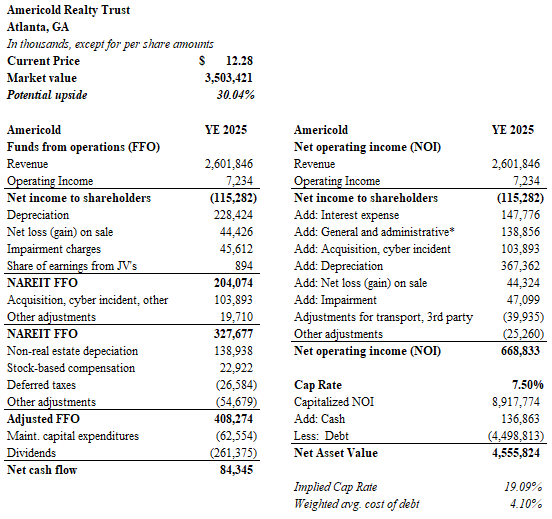

The point here is that you may think you can just evaluate a refrigerated warehouse portfolio as real estate, but you really need to factor in lot of management. Probably much more than you’d have in a net-lease industrial realty business. Let’s take Prologis, the biggest industrial landlord. In 2025, Prologis had general and administrative expenses of $469 million on $8.8 billion of revenue, or just about 5.34%. In contrast, Americold has $269 million of G & A expenses on $2.6 billion revenue. That’s almost double.

Why is this important?

Well, a lot of people use the exercise of applying a capitalization rate on net operating income (NOI) to arrive at value the underlying assets. NOI is a real estate cousin to EBITDA, and most REITs publish this number for us real estate hillbillies followers to consider. When they compute NOI, they add back general and administrative expenses. The theory here is that a buyer of the individual properties wouldn’t be burdened by the parent company’s management costs.

The casual observer might take the NOI for Americold at the end of 2025 and make the assumption that the assets are worth $13.3 billion. COLD published NOI of $800 million at the end of 2025, so $13.3 billion is what you get with a 6% cap rate. Let’s use 6%, since that’s about 200 basis points above the company’s current debt cost. Subtract debt of $4.5 billion and the net asset value could be $9 billion. The market cap for Americold is only $3.5 billion. Before you run to your Robinhood account, take a breath. Unfortunately, these assumptions are far too aggressive. Adding back $269 million of general and administrative expenses is not realistic. These are businesses as much as they are buildings, and sweeping aside a layer of management is simply not possible.

I decided to value the real estate using a 7.5% cap rate. Investors in institutional quality real estate would probably argue in favor of a lower rate, but I figure the current cost to borrow money is more like 5.5% and I’d still want to earn 200 basis points over that number. It’s also a soft market. As a general practice, I don’t think you should underwrite deals by penalizing them with the bigger cap rate. Rather, you should make the adjustments in your future rent assumptions. You may want to assume that revenues will fall by 10% for refrigerated warehouses given the oversupplied market conditions. Such a rent reduction would knock $260 million off the top line, and eviscerate $3.5 billion of value. Maybe the market knows this, and that’s why the chart for COLD looks worse than the Thwaites Glacier.

I don’t have time for a rent sensitivity analysis, nor do I know the market that well, so I will just use 7.5% as my cap rate in this exercise. Hypocrisy be damned.

Instead of adding back $269 million dollars of general administrative expenses, I added back $139 million. This number represents 5.34% of revenues, just like at Prologis. In other words, I’m saying $130 million of general and administrative expenses are an integral part of Americold’s business and can’t be removed for purposes of valuing the real estate. The resulting NOI is $669 million. Let’s capitalize that number at my 7.5% to arrive at an asset value of $8.9 billion. Less debt, the net asset value for Americold calculates to $4.5 billion. This is approximately 30% above COLD’s market capitalization. The market offers a decent discount, and it explains why Ancora Holdings has agitated for changes, including asset sales.

The 7% dividend yield is attractive and seems reasonably well covered if you believe management’s figures that maintenance capital expenditures amount to $62.5 million per year. This strikes me as a little on the low side, but I am just asking the question. I don’t have comparable data. I will say that refrigerated warehouses are filled with complicated cooling systems that require a lot of maintenance. Underestimate that number at your peril.

My verdict here is that a Americold presents a good value. The dividend seems like a solid way to earn some beefy yields while Ancora puts the company’s assets through their paces. Leverage is about 50% of my estimated value, so that’s a little high. One could envision a dividend cut if funds need to be marshalled for principal reductions. Fortunately, the company’s debt maturity timeline is long. The oversupply in the market will eventually be absorbed. I set Americold on the back burner for now, but I will likely revisit the business soon.

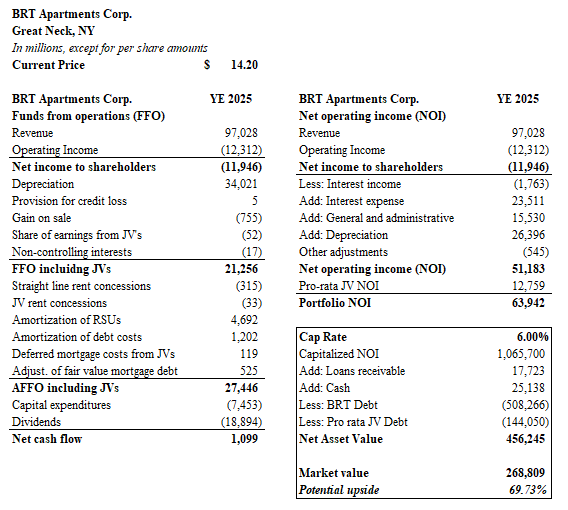

I have much more confidence in BRT Apartments Corp. The company is based in New York and owns about 5,400 units throughout the southeast. Many properties are held through joint ventures. The company is controlled by the Gould family. I have read various estimates about the amount of insider ownership at BRT, and it seems like it is nearly 95% when I toted up the 13-Fs. So, there’s not much float. No activists are going to come along and move the needle. The Goulds probably aren’t in a hurry to make any aggressive changes. The company’s dividend reinvestment program works in their favor. There’s no identifiable catalyst, in value investor parlance.

Despite these caveats, BRT is an exceptionally cheap stock. I owe a hat-tip to an Omaha fund manager. I would name him but I won’t, since I suspect he would like to add to his own position under the radar. The thin trading volume has meant that recent purchases have already pushed the share price above $14. It was $13.50 when I made my initial buys. The current market capitalization is $269 million, but I think the net asset value exceeds $456 million. BRT pays a 7% dividend yield – far higher than Avalon Bay $AVB and Mid-America $MAA. The assets are solid B+/A- apartment communities in dynamic metro areas. Yes, some of those markets have been fairly soft and the share discount may reflect some concerns about looming vacancy issues. The portfolio is also 60% leveraged, so there’s a riskier element to the business than some of the bigger multifamily REITs.

I’m not going to write a lot more here since I’ve already overstayed my welcome, but I will say that it is very hard to justify digging a hole for a new apartment complex right now when an investment like BRT is available as a public entity. One would be hard-pressed to generate a 7% cash-on-cash return today on most new developments using an equivalent percentage of leverage. With tons of money still out there chasing deals, the yield on most acquisitions would be even lower. BRT is certainly very attractive when compared to private market alternatives.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.