Commercial real estate is under pressure. Hospitality properties are in distress and many retail assets are struggling amid restaurant closures and the acceleration of online shopping. Thus far, long-term leases and high-quality tenant rosters have spared Class A office properties from pain. Second quarter results for major publicly traded office real estate investment trusts offer insights into the office markets of large cities, and their discounted stock prices appear to be attractive.

The second quarter results for three office REITs were reviewed for this report: Boston Properties (BXP), SL Green (SLG), and Kilroy Realty Trust (KRC).

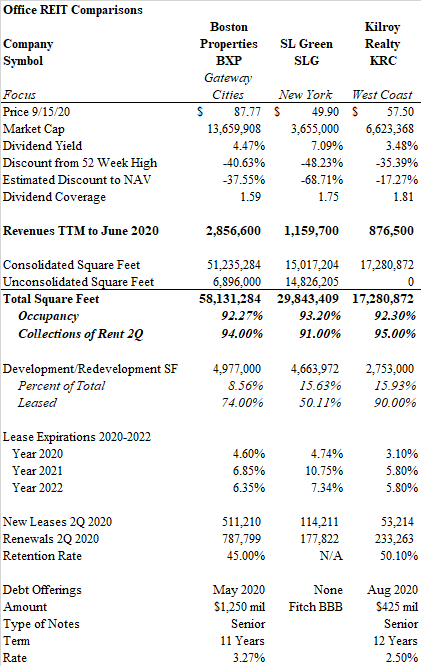

Boston Properties is the nation’s largest office REIT with over 51 million square feet owned directly, and another 7 million owned through joint ventures. BXP has concentrations of properties in New York, Boston, Washington, D.C., Los Angeles and San Francisco. SL Green owns nearly 30 million square feet in New York City with roughly half-and-half split between direct ownership and joint ventures. SLG also holds nearly $1.2 billion of mortgages, mezzanine loans and preferred equity positions in other New York properties. Kilroy Realty Trust has over 17 million square feet based on the west coast. It has a larger suburban portfolio than the others, and its stock has performed comparatively well.

All office REIT executives believe their companies are well-prepared to weather the shift towards work-from-home arrangements. They have raised capital at low interest rates and bolstered their balance sheets. Lease expirations are minimal in the near term. Stocks are trading at considerable discounts to underlying asset values and offer hefty dividend yields. The ability to sustain dividend payments for the next two years seems likely and the discount to net asset values offers downside protection. Technology companies continue to lease new space. However, clouds hang on the horizon. A reduction in office floorplans seems inevitable. Financial firms may reduce headcounts as they reckon with tighter interest rate spreads and a rising collection of distressed assets in their portfolios. Meanwhile, working from home may not prove to be the revolution once envisioned in April, but certain jobs will remain permanently remote.

Note: This paper contains the opinions and interpretations of the author. No representations are made regarding the accuracy of the material. The views do not represent investment recommendations. All readers should perform their own due diligence before making an investment decision.

Occupancy and Collections of Rent in the Second Quarter

All companies collected over 90% of rents during the second quarter. BXP suffered from vacancy at its hotel properties, and both BXP and SLG reported rent collections only slightly better than 50% for their retail square footage. Yet office rent collections were better than feared. BXP and KRC collected 98% of office rents and 96% of SLG’s office tenants paid during the second quarter. Overall occupancy at the end of the June period stood hovered near 93% for all three firms. However, the actual staff presence in the buildings was minimal, with only about 10-15% physical occupancy for BXP and SLG and 25% for KRC estimated during late July.

Financing

BXP and KRC took advantage of the decline in interest rates to raise significant capital during the past six months while SL Green sold two assets for over $600 million to bolster the balance sheet. In August, Kilroy raised $425 million in senior notes at 2.5% due in 2032, and Boston Properties issued $1.25 billion in senior secured notes at 3.25% maturing in 2031. Kilroy raised $247 million in a March share offering. No new senior debt was issued at SLG, although a couple of properties were refinanced. Fitch did affirm a BBB credit rating for SL Green but revised its outlook to “negative”.

Shareholder Benefits

All CEO’s believe that their balance sheets are well-positioned for the next two years. Kilroy increased its dividend by 3% in August and SL Green purchased $163 million of stock during the second quarter.

Leasing Activity

Despite the pandemic, leasing activity did continue at muted levels. All three companies renewed about 1.5% of their portfolio with an approximate retention rate of 50%. BXP signed a major new lease for 400,000 square feet with Microsoft at its Reston, Virginia property. BXP and KRC have minimal lease expirations over the next three years with KRC at roughly 4% per year through 2022 and BXP closer to 6%. Kilroy has 85% of its space concentrated in low and mid-rise buildings. SL Green has minimal exposure in 2020 but faces a worrying 11% expiration level in 2021.

Kilroy and Boston Properties are bullish on markets where technology and life science businesses are showing resilience and even growth during the pandemic. While Facebook, Google and Amazon grab the most headlines, the emergence of laboratory needs in the biotechnology and pharmaceutical industry is equally fascinating. These companies are viewed as more likely to take up new space in coming years as the office environment remains necessary to foster collaboration and company culture. Both firms show interest in the Seattle market while BXP seeks further growth in the technology hotspots near the Los Angeles beaches. A notable bright spot during the doom and gloom of New York City’s pandemic challenges was Vornado’s signing of Facebook to a 730,000 square foot lease in the former post office building near Penn Station.

Development Activity

All three REITs have significant development activity which accounts for between 9-15% of the total square footage inventory for each company. While these developments pose risk should they fall short of targets, all CEOs noted that they had adequate liquidity to finish the projects. 90% of KRC’s pipeline is leased while BXP has 74% leased in their upcoming projects. SL Green has higher leasing risk, as was cited in the Fitch ratings downgrade, with 50% of new square feet committed. Among all three companies’ projects in development, the most prominent is the 77 story SL Green tower known as One Vanderbilt – a 1.5 million square foot building near Grand Central Station which is 70% leased and opens this week. The project is a landmark $3 billion asset. The opening generated enough excitement to propel the stock upwards by over 10%. SL Green is also partnering with a Korean pension fund on the $2.3 billion redevelopment of One Madison Avenue. The space is not scheduled for delivery until 2024. Kilroy is in a strong position with its development projects. KRC will soon be opening a 355,000 square foot building in Hollywood fully leased to Netflix and another 635,000 square foot building in Seattle 100% leased to a Fortune 50 company. Another 285,000 square feet in San Diego will come online in 2021 with 91% of the space leased.

Sublease Risks

One of the factors most likely to suppress future rents is the likelihood that surplus space is placed on the market by current tenants. These subleases become phantom vacancy that is nearly always offered at below-market rents. CEO John Kilroy did not view the subleasing environment as overly worrying. In reference to San Francisco in particular, he offered, “Sublease space in the market right now is about 5 million square feet… 2.3 million was added during Covid… to put that into perspective, the direct vacancy rate in San Francisco right now is about 5.4% and sublease is 2.5% of that. To compare that to the dot-com bust, direct vacancy was 8.3% and sublease space with 6.8%.” However, despite the CEO’s comments, Kilroy identified sublease space in its 10-Q, the first time in several quarters such information was broken out. 849,000 square feet in the portfolio was listed for sublease, or nearly six percent of the portfolio. About half the space was noted as vacant. In late July, DropBox announced it would list 270,000 sf for lease, nearly 1/3rd of its offices, in the newly opened Kilroy development in Mission Bay, San Francisco. Meanwhile, Boston Properties was impacted by the bankruptcy of Ann Taylor’s parent company which occupies 340,000 sf in Times Square. It would seem likely that even if a bankruptcy restructuring is successful, surplus space will find it’s way onto the market.

SL Green Challenges

SL Green is the most difficult office REIT to analyze. Nearly half of the company’s square footage is held in joint ventures which are not consolidated in the operating revenues and expenses. The company also has a complicated portfolio of first mortgages, mezzanine loans and preferred equity positions in various properties in New York. SLG also owns many properties encumbered by ground leases.

Indeed, some mezzanine loan positions appear to be under pressure. On September 2nd, it was reported that SL Green bought the $90 million first mortgage for 590 Fifth Avenue after Thor Equities defaulted on a $25 million mezzanine note. The property is a 19 story 100,000 sf building. The mezzanine business cuts both ways for SL Green. A distressed developer who falls behind on their mezzanine financing could present an opportunity for SL Green to pick up assets for the value of the first mortgage. In most cases, these will be bargain acquisitions. Unfortunately, the impairment of a mezzanine loan is in itself a damaging blow to the balance sheet and the need to muster capital to protect a junior debt position could require deeper pockets than the company anticipates.

While two asset sales reinforced cash positions, the failed $815 million sale of the Daily News Building in March offered an indication of the challenges valuing New York office assets in a post-pandemic world after Deutsche Bank pulled financing for the deal. SLG was able to refinance the property in June with a $510 million mortgage from a lender consortium. SL Green is also considering the sale of its two multifamily properties.

Investment Evaluation

SL Green has seen its stock hammered by the pandemic. Down by nearly 50%, SLG’s dividend yield exceeds 7%. Boston Properties has faced a 40% decline and offers a yield of 4.4%. Meanwhile, Kilroy lost 35% since its pre-Covid highs and yields 3.45%

In the process of evaluating the stocks, I made simple assumptions. Some may argue that these are too elementary, but the exercise was intended to discover whether the public market is significantly undervaluing the underlying assets by a wide enough margin to provide an element of downside protection. I was not intent on arriving at a precise valuation of the businesses.

My method was to annualize pro forma income simply by taking second quarter revenues and multiplying them by four. This may prove generous in the event further occupancy problems arise; it also is punitive for the companies. For example, the methodology assigns no future income for the Mission Bay/DropBox property placed in service. It also ignores the 70% occupancy of One Vanderbilt placed in service by SLG. It gives no value to the new BXP leasing in Virginia. In all cases, the exercise merely values the development assets at cost. The only upside “help” that was given by the author was a slight uptick in hotel revenues attributed to BXP during the balance of two quarters.

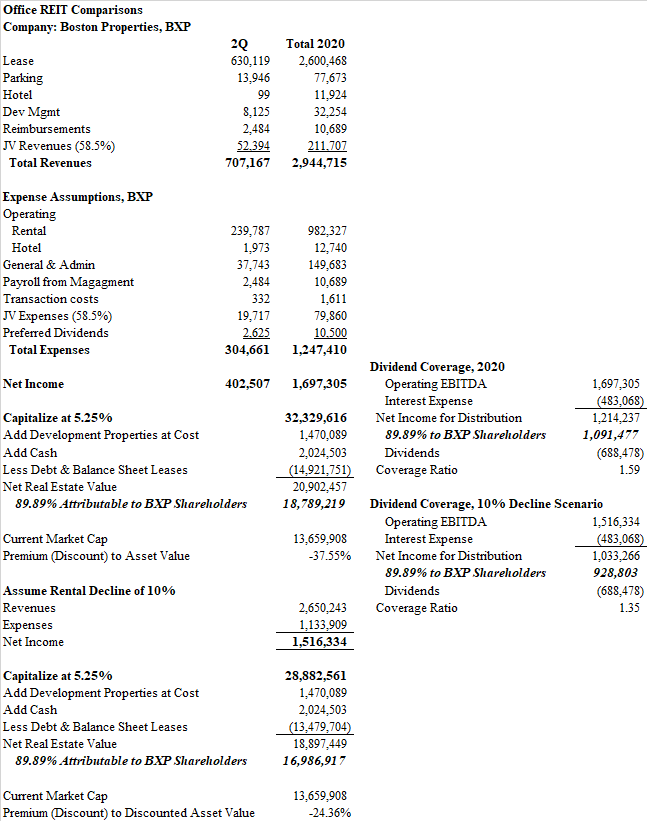

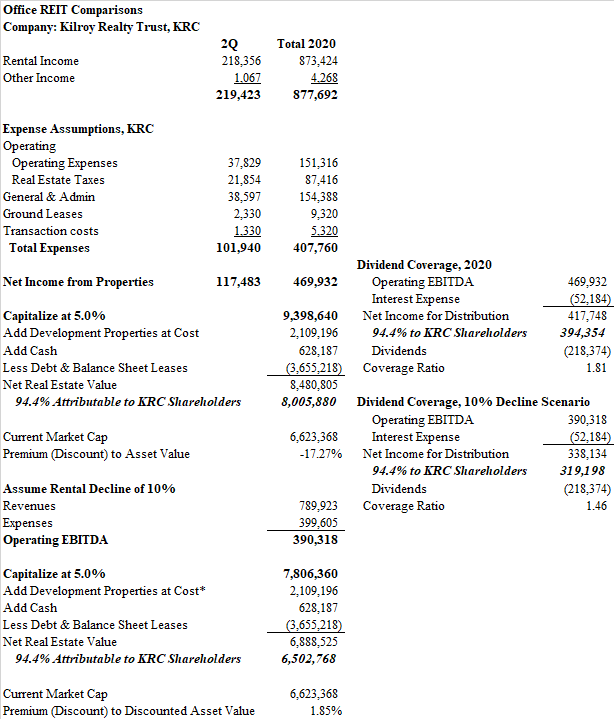

I capitalized the net income at 5.0% for KRC due to its high level of low and mid-rise buildings, 5.25% for BXP, and 5.5% for SLG. Certainly, before the pandemic, these cap rates would be considered high for trophy office properties in major urban areas. I added the cash on the balance sheet and subtracted debt to arrive at a net asset value. All in-progress development projects were added at cost. Joint venture assets were included in the income statement computations to the extent that they were reflected in the ownership percentages. The result is a 70% value discount for SLG, and a 38% discount for BXP. KRC is selling for a 17% discount. On the income side, I calculated the dividend coverage ratios: BXP stands at 1.6x, SLG 1.7x and KRC 1.8x.

Next, I performed a stress test analysis that reduced revenues by 10%. In the case of SL Green, I also deemed their property loan portfolio to be 50% impaired. Even with this penalty, SLG appears to trade at par to net asset value. Meanwhile BXP would seem to be 24% below value as well. KRC with its under-estimated future income looks to be valued at par after the stress test. In this example, BXP and KRC could continue to comfortably fund their dividends but SLG would be under pressure to reduce shareholder payments.

Paradigm Shift

While all three companies trade at steep discounts, one can’t help but wonder if the world will look back at this moment and ask why real estate experts underestimated the paradigm shift of working from home. If it worked pretty well for 6 months for most office workers, why can’t it work permanently? If nothing more, workers got 1-2 hours of their days back by not facing a long commute into the city center. This increase in productivity alone is tangible.

Of course, as the weeks have dragged on, frustration has set in with the arrangement. JP Morgan CEO Jamie Dimon has summoned traders back to their desks and recently noted a decline in productivity among employees at the banking giant. Zoom meetings can’t replace the 80% of communication that occurs through body language, and even a micro-second lag on a call is maddening after the third time someone interrupts. The office is a vital asset in our knowledge and information-based economy. Ideas and culture are the engines of growth. But data entry, call centers, accounting and routine back office functions seem to need nothing more than a good workstation in the den along with a high-speed data connection. Office leases will take 2-5 years to expire, but what if all companies simply reduced their footprints by 10%? My stress test may prove to be too light.

Conclusion

Kilroy and Boston Properties are the most appealing investments. The balance sheets have been fortified and leasing activity for the companies’ new developments is robust. Kilroy’s exposure to suburban markets offers a hedge against central business districts in major cities, and BXP has a well-diversified geographic portfolio. Meanwhile, despite the steep discount, SL Green appears to be the riskiest of the three REITs. The concentration in New York City is worrisome. While some may argue that the risk is reflected in the added discount, it is worth noting the SL Green executives had been appealing to investors as recently as the fall of 2019 that the stock traded at an unjustified discount of 25% to its peers. A risky mezzanine portfolio and the complexity of its joint venture arrangements could pose future challenges.

The most encouraging future for office properties lies in the technology and life sciences industries. Despite recent sublease announcements, Both Kilroy and Boston Properties are aggressively pursuing these vanguard companies with visible degrees of success. Meanwhile, the transformation of New York City into a technology hub is well under way. The question is now raised: can technology employment grow fast enough to replace the shrinking office needs of remote workers?

Bert Hancock, September 15, 2020

bert@alchemydevelopment.com

Appendix: Exhibits