Hold the mayo.

Kewpie Mayonnaise is a household staple in Japan. It was introduced to the country in 1924 after Toichiro Nakashima enjoyed the condiment during a visit to the United States. Today, Kewpie has been elevated to cult status. You can even visit the company “terrace” in Tokyo. Many Western chefs say it’s the best mayonnaise in the world. Kewpie is serious about its appeal beyond Japan and just opened a new production facility in Tennessee.

Japanese mayo uses only egg yolks, so it has a more yellowish appearance than, say, Hellman’s. Creamier and mellower than it’s US cousin, Japanese mayo receives a distinct character from the addition of apple cider vinegar and monosodium glutamate (MSG). The American version of Kewpie omits MSG. Purists say don’t bother. Go straight to the Japansese original for the best flavor. MSG gets a bad rap in the States, but aficionados rave that the addition of monosodium glutamate triggers the famous “fifth taste” known as umami.

Kewpie (2809.T) has a market cap of ¥481.8 billion ($3.34 billion). The company’s shares seem reasonably priced. The stock trades at an earnings multiple of 17 and an EV/EBITDA multiple around 8. Sales have grown better than 5% per year for the past three years.

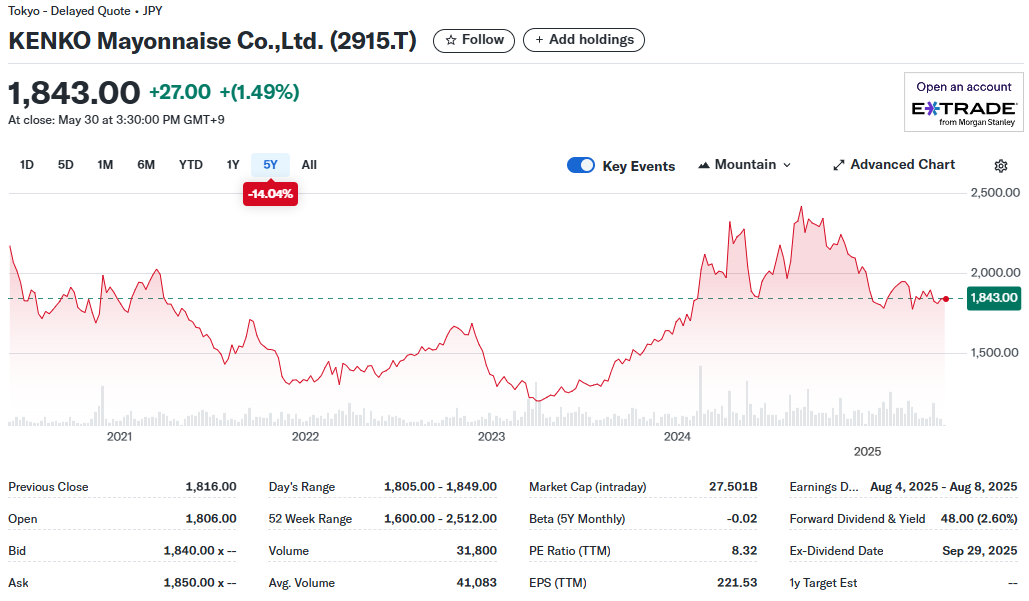

But Kewpie’s much smaller competitor is a better bargain. Kenko Mayonnaise (2915.T) is a distant second in the Japanese market with FY 2025 sales of ¥91.7 billion – less than a fifth of Kewpie. Kenko trades at ¥1829 for a market capitalization of ¥28.9 billion ($200 million).

The stock is very cheap, trading at an enterprise multiple of 1.5 times EBITDA. Kenko carries just ¥3.8 billion of debt and holds cash and securities of ¥21.3 billion. The stock has declined 23% from its 2024 peak. I believe Kenko trades at a market price that is half of its intrinsic value.

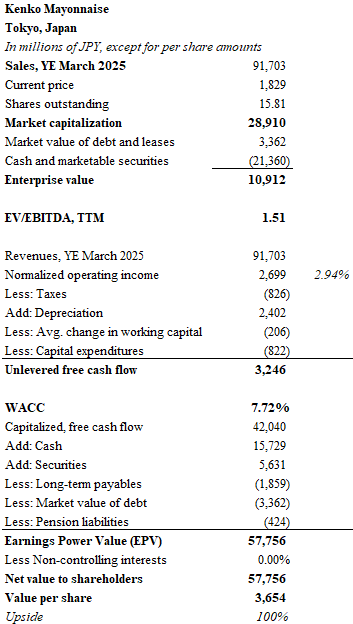

I performed a valuation of the business using an earnings power valuation method (EPV) which capitalizes free cash flow at an appropriate discount rate – the weighted average cost of the company’s capital.

First, I normalized operating income at a 2.94% margin which represents the average for the past five years. The resulting ¥2.7 billion of operating income was adjusted by subtracting taxes and adding ¥2.4 billion of depreciation. Next, deductions were made: ¥822 million for capital expenditures and ¥206 million for working capital. The sum of ¥3.25 billion is Kenko’s normalized unlevered free cash flow.

The denominator in the value equation is 7.72%, a figure representing the weighted average cost of capital. The market value of Kenko’s debt accounts for 10% of the company’s capital. Under current bond market conditions, the after-tax cost of debt is 1.78%. The cost of equity was computed at 8.4%. This represents a 6.91% premium to the current Japanese 10-Year bond yield of 1.5%. The capitalized gross value for Kenko at a weighted average rate of 7.72% is ¥42 billion.

Cash and securities were added to this amount, with deductions made for the market value of debt, pension liabilities and about ¥1.9 billion for long-term payables. The final EPV amounts to ¥57.8 billion ($400 million) or ¥3,654 per share.

The potential upside is 100%.

Too good to be true? Perhaps. Kewpie has a dominant brand, and it is unlikely that Kenko can increase market share without significant additional marketing expenditures. Kenko is a well-regarded product and it is popular in the Kansai region which includes Osaka, Kyoto and Nara, but it’s customers aren’t fanatics.

There’s also the problem with the aging domestic population. Japan’s population is shrinking. Kewpie has begun to carve a path to global growth, but the same can’t be said for Kenko. Where will growth come from?

Kenko has also suffered from erratic financial results. Operating margins have ranged from 5.3% in the most recent year ended March of 2025, to barely north of zero in FY2023. Returns on capital are in the low single digits.

I am also troubled by the possibility that Kenko’s free cash flow doesn’t accurately reflect the cost to maintain the plant and equipment. Depreciation is double the amount spent on capital expenditures. As Japan finally shakes off the curse of deflation, shouldn’t capital expenditure costs match or exceed depreciation levels?

Finally, corporations may finally be exiting the dark tunnel of deflation only to stumble into the harsh light of higher interest rates. Japanese yields have almost doubled since October, rising about 70 basis points. This is a stunning move. A massive unwinding of Japanese credit could lead to a serious fiscal reckoning and a recession. At the very least, higher rates could exert a gravitational pull on levitating stock prices.

Despite all of these concerns, Kenko still holds investment appeal. Kenko offers a wide margin of safety. Mayonnaise has become a central component of Japanese cuisine. Owning the second-best brand seems like a tasty choice… especially when its on sale.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.