I’m getting a little weary of Charlie Munger quotes, to be honest. Don’t get me wrong, there’s no question that we recently lost an intellectual giant and a man of high moral character. His investment acumen and the genius ability to cut straight to the heart of a matter was legendary. But I think the elevation of his aphorisms to a form of business gospel reduces our own capacity to think for ourselves. He was just a man. Mortal. It’s ok to have heroes, but it’s not safe to put them on pedestals.

I imagine Munger could be insufferable at times. A real crusty bastard. Did you ever see his dorm design for USC? He must have been a dynamo when he was earning his capital as a lawyer and real estate developer. You probably regretted getting in his way. He was unapologetic about his desire to be rich and I’m sure he never suffered fools gladly. Ah, but yes, at his core he was among the wisest of the wise. So, after a long-winded preface, here is my Charles Munger quote: “If something is too hard to do, we look for something that isn’t too hard to do.”

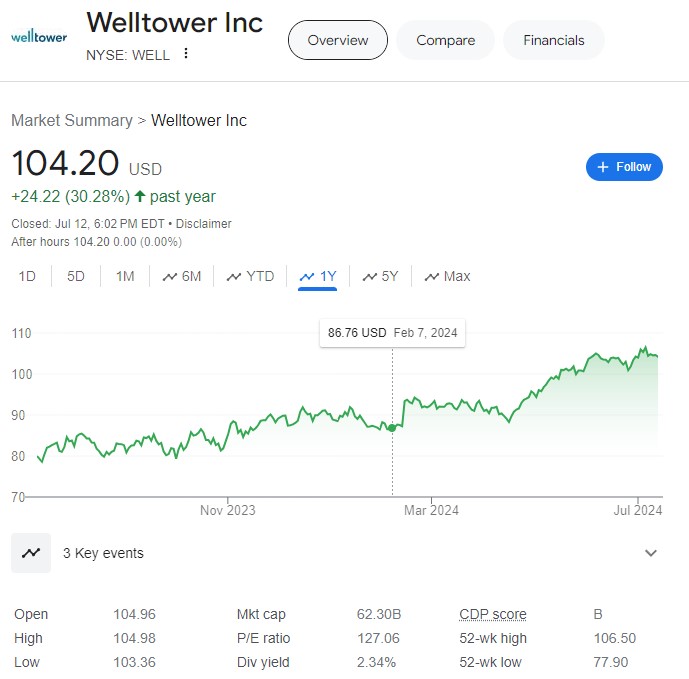

I’m filing Welltower in the “too hard” category. Welltower (WELL) is a $62 billion market cap REIT that owns senior living facilities and medical office buildings. WELL is also a bank of sorts. It lends money to developers of properties. It has JVs with a bunch of developers. Some of the assets are leased triple-net to operators, many are operated directly by Welltower. The company is also a prolific issuer of new stock and an expert at churning real estate. It’s head-spinning and hard to completely grasp. This is a company whose CEO, Shankh Mitra, quoted Jensen Huang in the annual report. I’m not saying that running real estate for old people doesn’t have much in common with NVDIA. Ah hell, who am I kidding? This is the vibes economy. Everything runs on NVDIA.

In fairness to Mr. Mitra, he also candidly told a 2023 audience, speaking of the industry, “On average, in the last 10 years we haven’t made any money for capital [providers].” The oversupply conditions of the middle part of the last decade were just beginning to recede when COVID hit. Now, prospects for better economics seem to finally be destined for senior housing operators due to the unfeasibility of new supply and the rapid aging of the boomer generation. The stock market seems to agree. The stock has run up 24% since the start of the year as occupancy and margins vaulted upwards.

Despite Mr. Mitra’s humility, there’s not much for me to like about the company as an investment. A REIT with a mixed collection of properties doesn’t deserve to trade at a higher multiple than apartment buildings, and certainly not better than medical office buildings. The demographic story has legs, I’ll grant you that. But you can say that about Skechers slip-ons or Hey Dudes.

I was first intrigued by Welltower late in 2022, when Hindenburg published a report questioning the absorption of some troubled JV assets. The short-seller specifically cast doubt upon the relationship with Integra Healthcare Properties. There was a lot of mystery about Integra. Hindenburg called it a phony transaction. Integra’s website is still just a collection of canned photos of smiling elderly folks with zero substance (at least they updated the copyright date to 2024!). Crickets from the market.

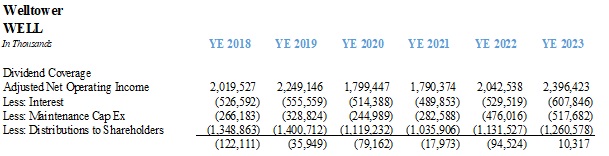

In my view, the only thing Welltower is guilty of is being exceptionally underwhelming. Welltower generated $6.4 billion in revenues during 2023. Property operating expenses absorbed 59% of revenues vs 52% of revenues in 2018. The industry sees itself getting back to pre-pandemic margins as staffing issues abate. I’m not so sure. States have ramped up calls for minimum staffing levels. The industry is also facing a lot of scrutiny about Medicare reimbursements. I don’t know enough about these challenges, so I can’t opine about the true risks to the company. I just know they exist.

What I can tell you is that I don’t think Welltower has much room to expand its distributions to shareholders above it’s current paltry yield of 2.35%. Once you deduct maintenance capital items from operating income and interest on over $15 billion of debt, there’s not much left.

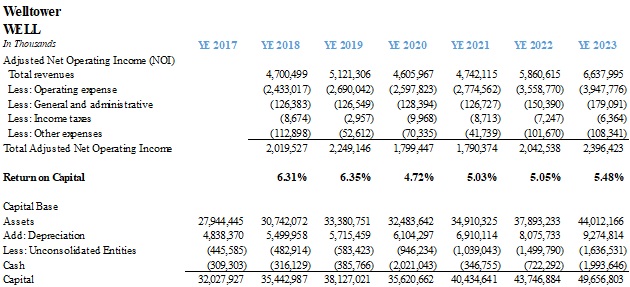

No matter how many assets the company churns, the return on capital seems mired in the mid-single digits. The company has issued over $14.4 billion of stock since 2018, acquired $18 billion of assets during the period, while selling $9.9 billion. All this huffing and puffing hasn’t produced a formula that shows it can distribute increasing levels of cash to shareholders in a sustainable way. It is not unfair to say that some of the distributions are being funded with new equity. That’s not a great recipe. And for a CEO that says there aren’t many opportunities for new construction, the deal guys didn’t get the memo because Welltower had about $1 billion of construction in progress at the end of 2023.

Apparently, the market completely disagrees with me about the Welltower story. A 25% stock increase for a senior housing play is impressive. I am equally impressed that Welltower just raised over $1 billion of new debt at 3.25%. Is it pure debt? No, not for Welltower. It’s another dilutive offering. A convertible note due in 2029 that vests once the stock price rises 22.5%. I’m not sure who buys such debt when the five-year Treasury yield can be had for 4%, but it was probably a couple of fund managers who were feeling as frisky as Wilfred Brimley and Don Ameche in swim shorts.

So, I bid you adieu, Welltower. Low returns on capital, poor coverage on a low dividend yield, a churn of assets, acting like a loan shark, pumping new stock and forming a lot of unconsolidated JV’s… sounds like this one’s just too hard.

The easy column. I missed a fat pitch. I looked at it and didn’t have time to get my bat off my shoulder. It may not be too late, but I still need to dig deeper. Hat tip to Adam Block on social media who noticed Peakstone Realty Trust (PKST) was trading around $11 per share on July 10, giving the REIT a market cap of about $382 million. It sported a dividend yield north of 8%. Alas, it ran up 20% in two days. It still trades well below the $39 per share of last summer, so there may be juice left in the squeeze.

Peakstone had $436 million in cash at the end of March with a book value of real estate (excluding depreciation) in the neighborhood of $3.3 billion. Yes, there is debt of $1.4 billion. It costs Peakstone about 6.75% to finance the loans which roll over during the 2025-26 period. So, there’s loan renewal risk as well. But this is a pretty good portfolio of assets. The buildings consist of office and industrial space, but they’re mostly leased to single users with high credit such as Pepsi Bottling, Amazon and Maxar. Total square footage of the assets is 16.6 million. Net operating income for the quarter was $47.6 million. As far as I can tell, the market was essentially ascribing zero value to the assets at the beginning of last week. Even if you figure a monstrous 12% capitalization rate on an annualized run of quarterly NOI, there is adequate cushion above the debt. Seems like one to dig into. Easy? No. Simple to comprehend? Yes.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2024-07-14 16:44:382024-07-14 17:22:39Too Hard

The Code of Hammurabi dates back to 1750 BC. These ancient laws contained the essence of the first banking contracts for managing loans. The farmer would borrow a bushel of seeds, reap the harvest, give the king about seven bushels of rye and keep three bushels for the family. In the modern parlance of Hammurabi’s descendant Jamiz ur-Dimon, a sound business endeavor earns positive leverage: the return on one’s capital investment should exceed the cost of borrowed money – the rate of interest. What happened if the loan required the farmer to pay back eleven bushels? It would probably end with the removal of a finger or three.

Business in the front, party in the back

As crazy as things got during the pandemic boom, the basic premise of positive leverage remained intact. Purchases of apartment complexes yielding 4.5% bordered on insanity, but at least lending rates could be found in the 3% range. Now, we have entered a strange, new post-pandemic era. Buyers of apartments have reduced their purchase prices in order to earn a higher rate of return on their capital. Low 5% levels are the reported “capitalization rates” that many buyers are willing to pay. This sounds logical until one realizes that the cost of fixed rate debt today is about 6%. Watch your fingers.

Why would a buyer accept such a meager deal? Three reasons. One, they are willing to earn a return on their own equity that is below the cost of debt. This seems nonsensical. Very liquid low-risk alternatives abound in the form of humble T-bills or, say, Chevron stock with a 4.2% dividend yield. Two, some believe interest rates will decline in the future. There are signs that such joy awaits: The Fed seems poised to reduce rates as inflation slowly approaches the target 2% level.

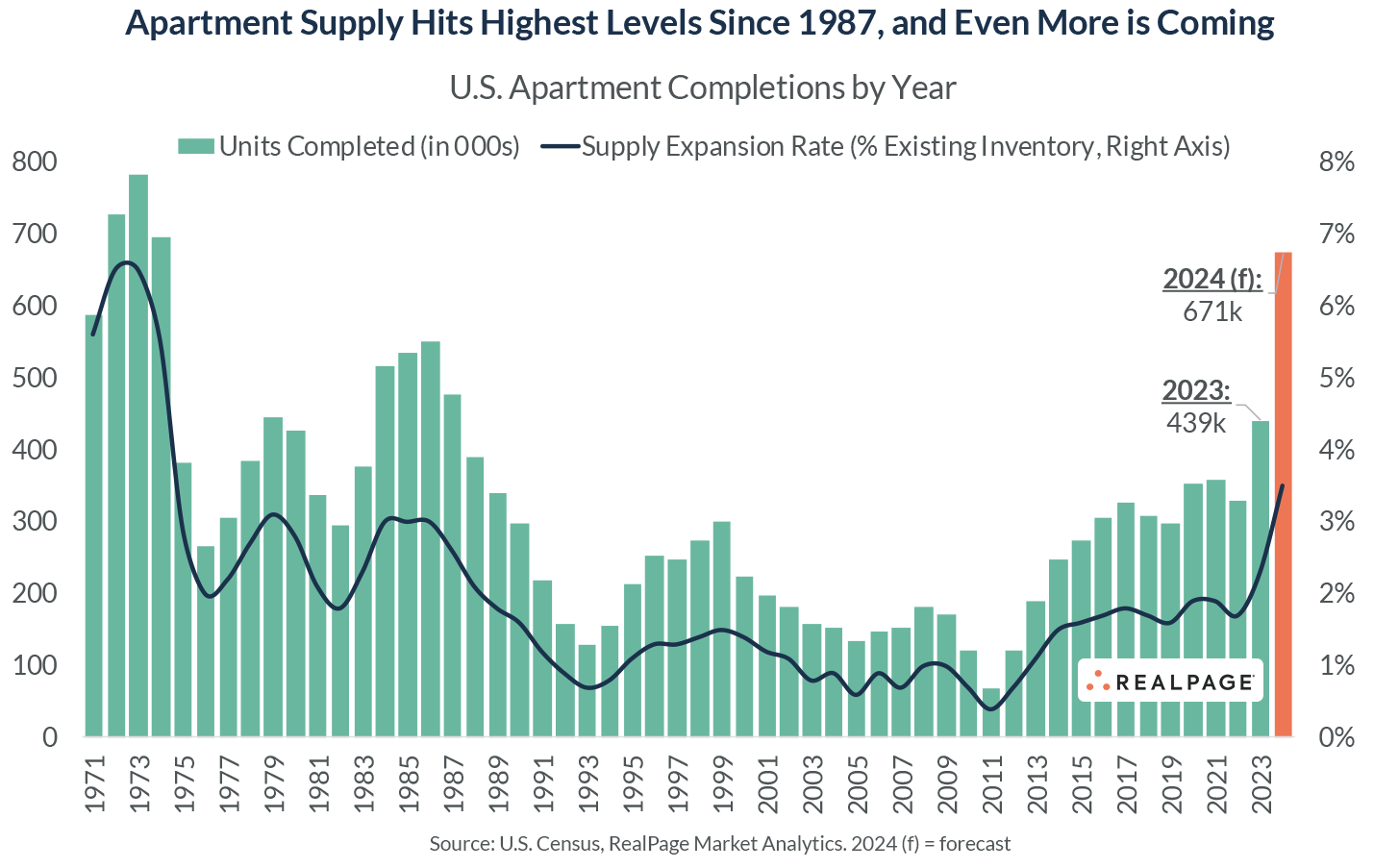

The third reason takes the opposite tack. There is a belief that inflation will lift rents faster than expenses in future years, and negative leverage will pleasantly reverse itself. This theory has merit. The greatest supply of apartments since the 1970’s is about to come to an end. Construction costs and interest rates have risen so high, that most new developments are unfeasible. Home purchases are out of reach for most Americans. The incumbents have a long runway to raise rents once the period of apartment oversupply abates. This is the theory behind KKR’s purchase of Lennar’s multifamily portfolio.

Flared trousers are back in style.

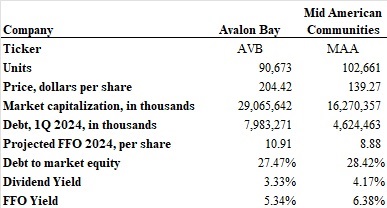

Publicly traded apartment real estate investment trusts (REITs) benefit from a low cost of debt and continue to earn positive leverage. Unlike their private competitors who must grovel for 6% permanent loan rates and 7% construction loan costs, the REITs have healthy balance sheets and can borrow at 5%. Mid-American Apartment Communities (MAA) and AvalonBay (AVB) are two of the largest landlords, and they are projecting returns of 6.5% on their (much reduced) development pipeline.

Both firms locked in low-rate long-term financing during the pandemic. Even as notes mature, healthy balance sheets at MAA and AVB provide pricing power in the bond market. In early January, MAA raised $350 million of debt at 5.1% for ten years – just slightly above a 100 basis point spread to the Treasury note. Assuming their development yields hold to projections and leverage is in the 30% range, they should be able to drive returns on equity to low 7% levels. Not fantastic, but sufficient to sustain dividend yields in the 3%-4% range and grow values in line with the broader economy. Both companies reported record low levels of resident turnover as home purchases have become less affordable.

Not everything is rosy for the REITs. The apartment supply hangover has arrived to pandemic boomtowns like Dallas, Atlanta, Houston and Nashville. Indeed, both MAA and AVB offered some sobering news: rents on newly vacant units were trending negatively in the first quarter. MAA, focused primarily on sunbelt markets, posted a negative 6.5% new lease rate. AVB was closer to negative 0.5%. Fortunately, high resident retention and rent increases of 5% on renewal leases kept the top line growing at both companies. Neither of these stocks is cheap. Taking projected 2024 funds from operations (FFO) – the preferred measure of operating earnings for a publicly-traded REIT – AVB trades at an FFO yield of 5.35% and MAA trades at a 6.43% forward FFO yield.

Meanwhile Farmland Partners (FPI) presents the perils of negative leverage. FPI owns and manages farms (177,000 acres) and has a market capitalization of $553 million. FPI shares peaked at $15 in 2022 and sit at $11.50 today. The dividend yield is a paltry 2.09%. Corn prices have round-tripped during the past five years from $4 per bushel in 2019 to $8 per bushel in 2021, and back to around $4.25 today. Not even Russia’s invasion of one of the world’s top grain-producing nations was enough to sustain wheat prices much higher than $6 per bushel.

You and Whose Army? Corn prices since 2019, Source: Macrotrends

Given these daunting agricultural prices, FPI doesn’t offer shareholders much value. The company generated $57.5 million in revenues in 2023 and had $31.3 million of EBITDA. The company spent about $25.6 million on interest and divdends to preferred shareholders, leaving just $5.7 million for common shareholders. This diminutive profit is not sufficient to cover the common shareholder dividends of $12.2 million.

FPI has been selling land to cover its dividend, and really, this is probably the best path forward – sell assets, reduce debt and retrench for the future. The floor on the stock is probably the market value of the land. A swag number of $6,000 per acre means there may be well over $1 billion of land vs $480 million of debt and preferred stock.

Positive leverage feeds your family. Negative leverage only feeds the king.

I remember watching the World Cup back in 2006. Italy won the tournament after Zinedine Zidane of France was sent off for headbutting Marco Materazzi in one of the most infamous moments modern football, er, soccer. The network must have thought Americans would get bored watching guys kick a ball around for 90 minutes, so they decided to scroll instant messages from worldwide fans across the bottom of the screen during several games.

Everyone remembers the headbutt and red card, but I remember a message on the screen. It was a Roma fan’s tribute to Italy’s beloved midfielder Francesco Totti that is forever etched in my memory. “Totti, Totti, Totti…We love him so much we name our dog Totti”. I don’t know what it was about this message of devotion to a piccolo cane italiano, but the little pooch earned a place in my heart. In my imagination, Totti is a gray Italian dachshund who loves to mangia soppressata. Oh Totti, ti amo.

I’m a day late. Already, my goal of therapy writing investment insights on a bi-weekly basis has gone the way of Monsieur Zidane – straight down the tunnel and into the locker room. But hey, rain or shine, we’re gonna walk Totti. Scrivi bene!

Who needs a meme when you can have a statue?

Before we get to the Totti of the matter, here’s a musical diversion that blew my mind. Seven Nation Army’s signature bass line is not from a bass guitar. It was actually played by Jack White on a Kay hollow-body guitar. According to Rick Beato, he used a DigiTech digital whammy pedal with the octave-down setting. Maybe I shouldn’t have been surprised. After all, Jack White is a masterful musician and the White Stripes were pretty much a drum/guitar duo. I never saw White Stripes live, so I had no reference point. Totti for you, my friend.

You like some Totti, you say? I think I have a couple of dividend ideas. Equity Commonwealth has a preferred yielding just below 6.5% and trades slightly less than the call price of $25. Equity Commonwealth was founded by the legendary Sam Zell to take advantage of commercial real estate bargains. Sadly, Zell passed away last year. Distress that he predicted in the industry was postponed due to all that pandemic juice. Present management sits on a cash pile of $2 billion and a handful of assets. They have said that if they can’t come up with a strategy to deploy the funds, they will wind down the business. The common is appealing, but the preferred is a fairly low risk way to park some cash.

A more adventurous dividend can be found in BCE, Inc. This is the old Canadian Bell. Like the AT&T of yore, it contains a lot of good (fiber optic and cellular networks, some tv networks), a lot of bad (legacy landlines, pension funds, debt), and some intangibles (37% of the Maple Leafs & Raptors, 20% of the Canadiens). The business is basically sound ($30 billion USD market cap) and the dividend is well-covered with a yield above 8.5%. The stock is down 50% since 2022 as government funds to boost the expansion of fiber optics networks were dialed back (pun for the boomers). They have curtailed capital expenditures and are laying off 9% of the workforce. I intend to do a deep dive on BCE because there may be some hidden value in a break-up and I like the positive Canadian demographic trend. I think you are adequately compensated for what is probably, at worst, a stagnant business. In a world of NVDA go up, 8.5% dividend checks sound like a snoozer but that’s where we be at. Vibes. 🔥

I took the Myers-Briggs test for the third time in my life yesterday. Wait for it. The first letter is an “I”. Shocking, I know. The rest of it actually was a surprise. I came in with an INTJ. Now, this made me well pleased. Uncle Warren is an INTJ. Zuckerberg, Musk? INTJ. F#%*ing Schwarzenegger is an INTJ! This is a small segment of the population. Rare air. Yes *silently pumps fist*.

I don’t recall exactly where I scored back when I took the M-B in my 20’s. I think it was INTP. Can’t remember. My Mom, a world-famous and passive-aggressive “I”, didn’t scrapbook those results. But this score contrasts sharply with my result from two years ago: INFP. I didn’t like that one. Too much feeling. Too many emotions. Now, it is true that some cool people are INFP’s. Creators. Bob Marley, John Lennon, Kurt Cobain, William Shakespeare, Johnny Depp. But not a lot of 4-star generals, Navy Seals, or NBA legends on that list. That’s probably not accurate. Dennis Rodman has got to be an INFP. You catch my drift here. Doris Kearns Goodwin isn’t pitching any biographies of INFPs to Penguin Classics. These are Oprah’s guests.

Questions naturally arise when you read the cast of characters. Did Arnold Schwarzenegger really sit for a Myers-Briggs exam? Did William Shakespeare truly prefer a quiet pub lunch with his mates to the crowded midsummer fayre? I am now on a search for the deeper meaning behind these two personality test results. INFP? INTJ? Who am I? Can I be both? Can I have Bob Marley’s soul and Zuckerberg’s bank account? It doesn’t work that way. Sorry. Or maybe it does? Maybe we are all coins with two sides? Janus with two faces. Jesters with two masks. Totti the man…Totti the dog.

Florida panhandle beaches are some of the finest in the world. Pristine white powder. Pensacola is not the kind of place I wanted to visit for lessons about the fleeting nature of human existence, yet there I was. Life is full of cruel twists and turns. Throw the genetic dice often enough and someone you love (maybe even you) will roll snake eyes. It’s not fair.

Philistines are met by the Holy upon arrival in Pensacola. Bible-clasping gentlemen stand on four corners proferring salvation to drivers. Can a young man in a white shirt and black tie with perspiration rings forming under the sleeves reach a sinner with averted eyes at a red light? Does it ever work? Does anyone ever turn into the Dollar General parking lot to ask for directions to the on-ramp of righteous eternal existence? One is all it takes. One driver. One soul.

If you’ve read this far, you may be thinking, “Death and salvation? Is this guy always so serious?” The answer is “hell, no”. I just sat down to ponder the weighted average cost of capital and this is the weighty path I took. I offer no salvation, no divine guidance. I’m not even very good with Google maps. But I decided to stand on a corner for the first time in a long time. Pen in hand. It’s good for my soul.

Mortality can be a pretty good business if you’re a skilled actuary. Promise to hand someone a large pile of dollars in the distant future in exchange for small cash payments over many years. Find enough healthy mortals to make lots of small payments, and immense wealth can be generated by investing these premiums before you have to return the piles of cash. The life insurance industry is really just about winning at the game of death. Outlast your policy holders and beat the clock. There are no Luka Doncic three-pointers at the buzzer on the court of life insurance. That’s because there’s no buzzer. The best life insurance companies tick along perpetually with Swiss precision.

Mutual of Omaha has been very good at the business of reinvesting insurance policy premiums. I decided to take a look at their most recent public financial reports. The venerable institution had over $9.6 billion in cash and invested assets at year-end 2023, and nearly $4 billion of policy holder surplus. I wanted to look at their financials to see how they are paying for the largest development in Omaha: the $650 million skyscraper that will soon become the tallest building on the horizon. I learned a few things reading their report:

Similar to most real estate developers, a big slug of leverage is invloved: At March 17, 2023, “the Company entered into a $550,000,000 senior unsecured credit agreement that is available for purposes of funding the new home office building.” In real estate terms, Mutual of Omaha is just like Bruce Dickinson – they put their pants on one leg at a time.

The bond bear market has not been kind to the fixed income portfolio. The worst sell-off of bonds in a generation left Mutual of Omaha with over $526 million of gross unrealized capital losses.

Mutual of Omaha has $214 million of short-term outstanding borrowings from the Federal Home Loan Bank. This represents a significant increase from the $40 million borrowed at the end of 2022.

I don’t know that many conclusions can be drawn from these observations. Personally, I would not have sunk 7% of my investable assets in a building that will likely be worth 20% less the day it opens. But Mutual of Omaha is a perpetual financial insitution, not a cyncial and balding middle-aged guy with a computer and a finite time horizon. They will hold the asset for longer than its depreciation schedule and it is an emphatic statement of corporate strength. In other words, $650 million is a fair price to pay for permantently establishing your image as a solid financial giant when such an image is essential to your brand. There’s a reason why Louis Vuitton sells bags in a palace on the Champs-Elysees instead of a Carrefour in Nanterre.

Second, the losses on the bond portfolio present no threat. Unrealized losses are actually much improved from 2022 when they amounted to over $690 million. Mutual of Omaha matches its investments to its policy obligations and they epitomize the definitition of “held-to-maturity”. There is no risk of an imminent loss of capital. There is a downside, however, in the form of opportunity cost. $500 milion could be earning 2-3% more per year. Instead, Mutual of Omaha has to let those underwater bonds mature. Because the only thing worse than unrealized losses are…realized losses. It’s just the sort of income you might wish you had available if you were to, say, pay for a new office building.

Finally, the Federal Home Loan Bank borrowing raises some concerns. The FHLB window was opened wide last spring when some banks ran into liquidity issues. Are there liquidity issues in the Mutual of Omaha portfolio? It seems unlikely, yet the $175 million increase didn’t suddenly materialize out of nowhere. Calls were made. Flesh was pressed. Deals were done. Frankly, I did not even know that insurance companies could borrow from the FHLB. This was news to me. Apparently $134 billion has been loaned to insurers, and the low cost of funds present a wonderful arbitrage opportunity. Imagine that. A taxpayer-backed hedge fund mechanism. I’m not sure how I feel about being the backstop for more leverage in the housing system. But as the saying goes, “Teach a man to arbitrage…”

So, there you have it. Dante might be proud. We started our little story with damnation and ended with a cursory look at the financial results of an insurance company specializing in death benefits. As a wise man once sang, “Don’t fear the reaper.”

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2024-05-29 22:22:132024-05-30 02:39:08Preaching to the converted

For a moment today, the three-month United States Treasury Bill offered a yield higher than what could be earned by loaning the government money for ten years. Prepare accordingly.

Congratualtions to Barb! She is leaving Alchemy Development and joining a leading engineering firm in Omaha. Barb joined Robert Hancock & Co. in 2004 and went on to manage construction projects including Pinhook Flats, Cue and Shadow Lake Square. She has been an outstanding partner and her experience and wisdom will surely be missed. We wish her all the best on her new journey.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2022-07-31 21:34:252022-07-31 21:34:26Best wishes to Barb Terry

Jim Chanos, the famous Wall Street cynic, has cast a wary gaze upon real estate investment trusts that own large data centers. “This is our big short right now,” Chanos told the Financial Times. He has no doubts that cloud computing will continue to grow, but he believes that companies like Digital Realty Trust (DLR), Equinix (EQIX), and CyrusOne (CONE), are destined for trouble. His thesis: Amazon Web Services, Microsoft Azure, and Google Cloud will increasingly bypass the REITs to scale their operations by building data centers of their own. “The real problem for data center REITs is technical obsolescence,” said Chanos. “Their three biggest customers are becoming their biggest competitors. And when your biggest competitors are three of the most vicious competitors in the world then you have a problem.”

Chanos has a long record of success betting against overvalued businesses, but his assessment of the industry contrasts with Blackstone which recently purchased QTS Realty Trust for $10 billion. Meanwhile, Bill Stein, the CEO of Digital Realty Trust, quickly countered Chanos’ comments by pointing out his firm’s record bookings for the first two quarters of 2022. Yet the changing dynamics of the industry were on display Tuesday when FedEx announced that it will save $400 million annually by closing all of its data centers to move completely to the public cloud.

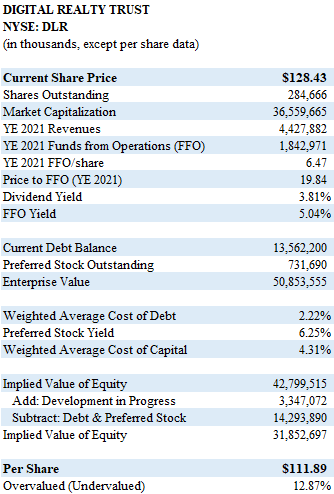

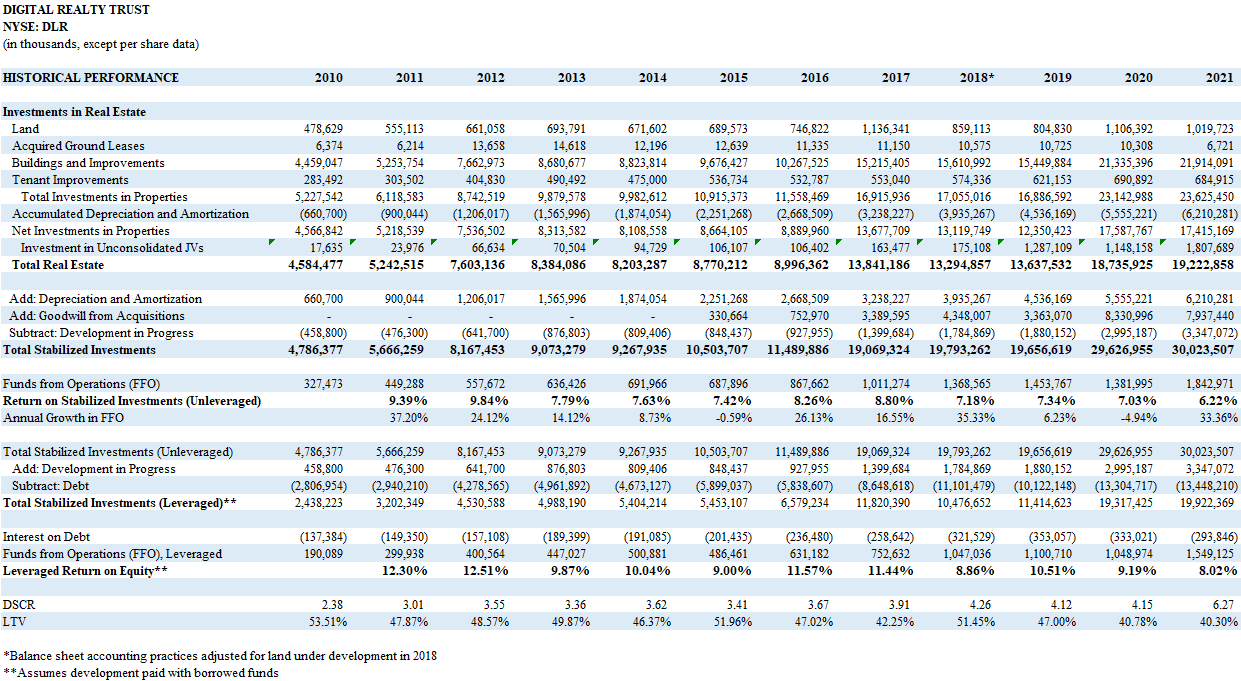

My rudimentary analysis of Data Realty Trust (DLR) indicates that the stock is overvalued by 10-15% relative to its underlying real estate. This kind of premium is uncomfortably high, but I’m not exactly grabbing my drumsticks for a round of Pantera. After all, the company has grown net operating income (or funds from operations, in REIT parlance) by 15% annually.

Despite the growth, there isn’t much appealing about a stock with a 3.8% dividend yield when you can earn 3% from 2-Year and 5-Year Treasury Notes. A business staring at such formidable competition should require a spread better than 80 basis points. A 25% drop in the price of the stock would be needed to produce a 5% yield.

Statistics for Digital Realty Trust are presented below. The table demonstrates a valuation of its real estate assets by capitalizing 2021 funds from operations (FFO). I add development in progress at cost and subtract debt to arrive at a net asset value of $111.89 per share, which is about 13% below the price on July 7, 2022. One could argue that I should employ forward estimates of FFO for my computation, and this would be fair. However, I am using a very low capitalization rate of 4.31%. This reflects the company’s low borrowing costs (2.22%). The FFO yield was used as a proxy for the cost of equity.

The second table shows results for the past 12 years. It indicates the rapid growth in net income for DLR, but it also shows that returns on total invested assets have been declining for years to levels below 7%. The low interest rate environment of the recent past juiced returns on equity, but even these results have become less impressive in recent periods. DLR has debt of about $13 billion on roughly $30-32 billion of assets, so the business is not exactly shy about using leverage. However, cheap debt acquired during the pandemic provided ample FFO debt coverage at 6.25x interest during 2021.

I don’t see a compelling reason to invest in DLR with the stock price trading above net asset values. And even though Jim Chanos may be hyperbolically talking his book, the threat posed by Amazon, Microsoft and Google is very real. Meanwhile, the dividends aren’t sufficient when the comparable safety of 3% Treasury yields beckons.

Note: This article contains the opinions and observations of the author. No investment recommendations are being provided and no representations are made to the accuracy of the content presented.

https://www.alchemydevelopment.com/wp-content/uploads/2022/07/Servers.jpg10811920adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2022-07-07 23:13:562022-07-08 02:44:15Data Center REITs Look Like A “Big Short” To Jim Chanos, But What Do The Numbers Say?

During the pandemic months of 2020, I sought guidance about apartment industry trends from the earnings reports of major apartment real estate investment trusts. The REIT stocks had fallen by about 35% from their pre-pandemic peaks, yet the CEOs struck me as fairly optimistic about their levels of renter demand. AvalonBay (AVB), Mid America Apartment Communities (MAA) and Equity Residential Trust (EQR) had all taken the opportunity to refinance debt in the 2% range and their dividends seemed safe. In the case of MAA and AVB, they were especially bullish on Sunbelt state demographics. Although urban properties experienced weakness (particularly for EQR), suburban locations were booming. The stocks rose significantly. By the end of 2021, MAA’s share price had doubled.

In hindsight, the massive amounts of fiscal and monetary stimulus introduced to the economy during 2020 and 2021 were generous gifts to the housing industry. It now seems apparent that these measures exceeded the output gap in the economy caused by the pandemic. Central banks are now facing extraordinary inflation pressures exacerbated by the Russian invasion of Ukraine. On April 21, 2022, Fed Chairman Jerome Powell said the job market was “too hot” and that a 50-basis point rate hike was “on the table”. Since that date, the Wilshere US REIT index has fallen 14%.

Memorial weekend offered me a chance to survey the REIT landscape once again. I present some nuggets from various companies below. This is my own research and interpretation of results, and my commentary should not be considered investment advice.

AvalonBay (AVB): A turn towards lending

AVB owns about 80,000 multifamily units and has a market capitalization of $29 billion. The dividend yield is 3.02%. AVB posted a healthy 15.9% increase in funds from operations (FFO) during the 1st quarter of 2022. The REIT continues to focus on developing new projects in the Sunbelt’s highest-growth metro areas. Five new projects representing about $700 million in investments are currently in lease-up at yields of 6.1%. The company estimates that its $4 billion development pipeline will have a yield-on-cost of 5.5%. Meanwhile, AVB exited 3 assets in the New York metro area during the quarter at a weighted average cap rate of 3.9%.

These development yields are probably satisfactory in a world where bonds still yield less than 3%, but AVB has calculated the math and decided that lending to other developers may be more profitable. AVB has established the Structured Investment Program to make mezzanine loans and preferred equity investments. They aim to grow the pool of capital to $500 million in 2-3 years. In addition to an expanded line of credit, AVB plans an equity share offering as needs arise in the amount of $495 million. AVB figures that mezzanine debt earning 8-12% is a low-risk way to deploy its cheap cost of capital. The Structured Investment Program isn’t a massive change of direction, but it would seem to indicate that runaway cost inflation has narrowed the opportunities to generate significant shareholder gains from development.

AVB has declined by 22.5% since it’s April peak, yet the company (along with MAA) remain the best ways to invest in the long-term Sunbelt demographic housing story.

I was intrigued by the 5.89% dividend yield available to shareholders of LTC Properties at current market prices. LTC has a market cap of $1.52 billion. LTC invests in seniors housing and health care properties primarily through sale-leasebacks, mortgage financing, joint-ventures and structured finance solutions, including preferred equity and mezzanine lending. LTC’s investment portfolio includes 202 properties in 29 states with 33 operating partners consisting of real property investments, first mortgages, mezzanine loans, working capital notes and unconsolidated joint ventures. Based on its gross investments, LTC’s investment portfolio is comprised of approximately 50% seniors housing and 50% skilled nursing properties.

My interest in LTC didn’t go far. Although occupancies continue to improve from the challenges presented during the pandemic, several operators in the portfolio remain under pressure. LTC, like AvalonBay has increased its focus on mortgage financing and mezzanine lending to operators and developers of senior housing. The rates charged to the developers and operators are well in excess of 7%, so the company should be able to leverage its balance sheet. Two weeks ago, LTC raised $75 million in senior unsecured notes at 3.66%. The company has a strong tailwind of demographics at its back, and occupancy should continue to recover. On the other hand, one must wonder about the credit quality of the operators in need of financing between 7.5% and 10% versus conventional bank loans.

The entire skilled nursing industry is facing tremendous pressure. Since the start of the pandemic, the skilled nursing industry has lost 241,000 workers or 15.2% of its total workforce. Wendy Simpson, CEO, also raised concerns about the efforts by Medicare to reduce reimbursement rates for skilled nursing. Last month, the Centers for Medicare and Medicaid Services (CMS) announced a $320 million cut in the reimbursement rate. This will undoubtedly put pressure on marginal operators. There is possibly an argument to be made that the stock has priced in these challenges, and LTC could capitalize on distress to increase its market share.

Blacktone’s REIT: Premium properties…at a price.

Blackstone (BX) has been aggressively growing it’s REIT over the past two years. BREIT has about $102 billion of assets and a net asset value of $66 billion. The annualized distribution rate is 4.5%. It is a non-publicly listed real estate trust that requires investors to be accredited, however the bar to invest is low – $2,500 is the minimum purchase. Fifty percent of the assets are concentrated in the residential sector and BREIT now owns 232,000 units including a massive portfolio of single-family rental homes. In July of 2021, BREIT purchased the 18,909-home inventory of Home Partners of America for $5.9 billion. BREIT will also become a major player in university housing by purchasing American Campus Communities for $13 billion. The deal was announced in April. Industrial represents 29% of the portfolio. BREIT also owns the net leases for the Mandalay and Bellagio hotels in Las Vegas and recently concluded the purchase of the 3,000 room Cosmopolitan through a joint venture.

Blackstone’s REIT offers investors a chance to earn a good yield on some of the finest real estate in North America. The share price is pegged to the net asset value, so an investment in BREIT should be insulated from the whims of the public markets. Blackstone has one of the most talented teams in the industry and can use its enormous balance sheet to uncover unique investment opportunities. However, an investor in BREIT needs to be aware of the fee structure. It isn’t cheap. There is a 3.5% broker commission fee and a 0.85% annual stockholder servicing fee. Blackstone, as the Adviser, receives a management fee calculated at 1.25% of net asset value. Finally, the Special Limited Partner (Blackstone) is entitled to 12.5% of the upside in NAV over a 5% hurdle.

The performance participation fee can be very large. In 2021, it amounted to $1.37 billion on revenues of $3.7 billion. The Special Limited Partner opted to receive this compensation in the form of shares at the end of December 2021. In January, a portion of the shares were redeemed for $566 million. In fairness, the massive scale-up in operations during 2021 and the cap rate compression that occurred during the year created a windfall that is unlikely to be as large in the future. The provision also contains a “claw-back” and “high water mark” condition which means that any declines in net asset value essentially subtract from the ability to earn the fee in the future. The fees are also not excessive when compared with what a private investor would face in a typical private real estate syndication transaction.

Due to the fee structure, investors should look at BREIT the way they would evaluate a private property acquisition: plan to hold the investment for longer than five years and let the Blackstone machine do the heavy lifting. I would also use BREIT as a sort of private property investment gut check. When evaluating investment prospects, Charlie Munger often asks himself, “Can it beat Wells Fargo? Can it beat See’s Candies?” In this case, ask yourself, “Can the deal I’m looking at for Shady Lane Apartments beat Blackstone’s REIT”? Lately, the answer is usually… “probably not”.

Broadmark Realty Capital: Cheap for a reason?

Another REIT that captured my attention was Broadmark Realty Capital (BRMK), a mortgage lender with a dividend yield of 11.44%. The market cap of the company is about $975 million and the stock is down by nearly 29% over the past year. BRMK makes construction loans, bridge loans and land development loans. Their website boasts the “Highest Degree of Leverage” with the ability to “loan against the completed value of your project, with no loan-to-cost requirements.” At the end of the 1st quarter of 2022, the loan portfolio had a weighted average interest rate of 10.4% and weighted average maturity date of 18 months. BRMK requires that their loans do not exceed 65% of estimated completed value.

BRMK had about $97 million of cash on its balance sheet at the end of the quarter, largely the result of $100 million of proceeds raised from an unsecured debt offering in November of 2021 at 5%. The company has about $931 million in loans on its balance sheet against the only debt of $100 million in unsecured notes. Apartments and senior living account for about 19% of the assets. Residential lots and single-family homes make up another 12% each.

It was unsettling to read that BRMK has over $186 million of loans in contractual default at the end of the 1st quarter of 2022. The company also has about $63 million in real estate assets on the balance sheet from foreclosures. BRMK has the ability to raise $200 million through at-the-market share offerings but has not issued any new shares through the end of the first quarter. It seems very possible that the market is pricing in a dilution of shareholders, or a dividend cut. Either way, loaning money to developers at high interest rates sounds like a great business, until it’s not.

Bert Hancock, May 31, 2022

Note: This article contains the opinions and observations of the author. No investment recommendations are being provided and no representations are made to the accuracy of the content provided.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2022-05-31 21:08:452022-07-07 23:10:11REITs are down by 14% since April. What’s going on?

“Grief is nature’s most powerful aphrodisiac” – Chazz Reinhold (Will Ferrell), Wedding Crashers (2005).

Back in 2005, I watched in disbelief while apartment leases were being broken left and right as residents began to purchase homes at a frenzied pace. While the economy boomed, the apartment industry suffered. Now, some have begun to whisper about the formation of a new bubble stimulated by the zero-rate environment established by the Federal Reserve to prop up an economy battered by the pandemic. In a surreal world where low wage service workers struggle to pay rent, more affluent renters have the sugar rush of cheap money to feed a new home-buying surge. Throw in a desire for more space to work from home and host dinner guests in the backyard, and buying a house… well, as Owen Wilson would say, “just, wow”.

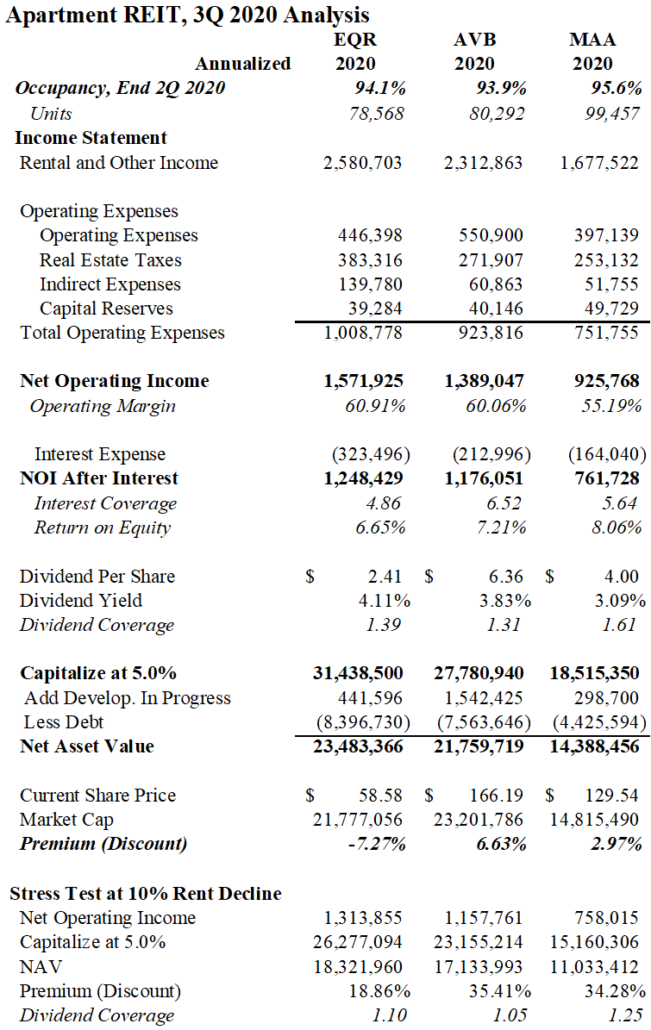

Back in August (which was eight months ago in pandemic time), I decided to look at quarterly results from publicly traded apartment owners to gain insights into where the market was heading. Third quarter results have been posted, so I revisited three of the biggest apartment real estate investment trusts: Equity Residential (EQR), AvalonBay (AVB) and Mid-America Apartment Communities (MAA).

The stocks have continued to trade at discounts to their

March peaks and their dividend yields exceed 3%. The announcement of a vaccine

breakthrough earlier this week sent the stock prices higher by 10%. The recent

price increases have largely erased the deep discounts to net asset values, but

they remain attractive as liquid income-producing investments. Their dividends

are well-funded, leverage is manageable, and it is hard to envision further

downside. EQR is the riskiest of the three because of the company’s high

exposure to struggling urban markets, but MAA remains the star of the group due

to its focus on sunbelt cities.

The attached article contains brief comments on the quarterly results, a numerical comparison of income and asset values as well as a back-of-the-envelope “stress test” to determine the safety of the dividend payments. Finally, I offer a few observations on the Omaha market where home purchases have caused increased turnover and vacancy.

Sunbelt Success Continues

Mid-America exhibits the divergence in the apartment

industry: urban coastal cities are losing residents and many are relocating to

dynamic growth centers in the south. As they had in August, executives exuded

confidence in their quarterly call. Occupancy exceeded 96% and traffic was

positive. Rent growth was muted due to increasing supply and competition from

home purchases but remained positive. MAA is a standout performer because of

its concentration in sunbelt cities throughout the southeast and Texas. The

stock has nearly recovered its losses for the year.

Suburban vs. Urban

AvalonBay and Equity Residential noted positive leasing

trends during October but reported that rent declines and move-outs exceeded

expectations in urban markets, particularly Manhattan, Boston, and San

Francisco. Rent declines surpassed 10% in big coastal cities. Occupancy dropped

below 90% in central San Francisco – a stunning figure. Meanwhile suburban

properties performed well. Overall occupancy at both firms was at the 94%

level. At AvalonBay, rents declined 6% for the quarter on a year-over-year

basis and 2% on a sequential quarterly basis. At EQR, rents declined 7.5% for the quarter on

a year-over-year basis and 2.7% on a sequential quarterly basis. Collections

remained strong – above 97%, but turnover increased. There were some glimmers

of hope in the New York City core where major rent discounts and incentives have

enticed bargain-hunters to seek upgrades within the market.

Similar Trends in Omaha

In large measure, the observations made by the leading

apartment executives on their earnings calls mirror our experience in Omaha.

Occupancy levels which had been above 95% for the past two years have fallen

dramatically over the past 90 days – approaching 93% in many areas of the city.

Effective occupancy may be even lower as one month of free rent has become a common

incentive.

Home Purchases Pressure the Top End

The top end of the Omaha apartment market has been hammered

by an acceleration of home-buying. Low interest rates are spurring a race to

purchase houses despite rising costs amid a tight inventory and expensive

lumber prices. There is a 2005-feel to the environment with a high number of

lease-breaks. It has not reached a mania level, but loose credit has allowed

buyers to emerge who probably wouldn’t have qualified for a mortgage at the

beginning of the year. In certain submarkets, added new apartment supply is

also depressing the leasing environment.

More Space

All three firms have noted an increase in demand for larger

apartments as working from home seems to have spurred a choice for bigger

apartments. Studios are difficult to rent across the country, and Omaha is no

exception. EQR reported that many of their Manhattan buildings have experienced

transfers to larger units within the same property.

Students and Lower-Income Challenges

EQR and AVB reported serious challenges in their Boston and

Cambridge properties due to a lack of students in the area. Omaha is no

different. Although UNO has strong enrollment figures, many have opted to

remain at parents’ homes. International students are a major driver of central

Omaha apartment demand, and they have not returned. Rent delinquencies had

vanished over the summer, but have made a growing re-appearance as stimulus

payments have been exhausted. Workers in the service sector are seeking

assistance once again. Delinquencies are not catastrophic – probably running

1%-2% higher – but the trend is worrying.

Stress Test

Last quarter, I used a hypothetical 5% income decline to

determine whether the firms could continue to fund their distributions. I

increased the pressure to 10% this time around. The dividends appear safe but

would certainly come close to being curtailed in such a scenario. It should be

noted that the 10% reduction of rental income was taken from an annualized rental

figure that already incorporates two quarters of rental declines. The

annualized figures are simply the aggregation of results through September 30,

2020 plus an assumption that 4th quarter results will match those of

the 3rd quarter.

Note: This article contains the opinions and

observations of the author. No investment recommendations are being provided

and no representations are made to the accuracy of the content provided.

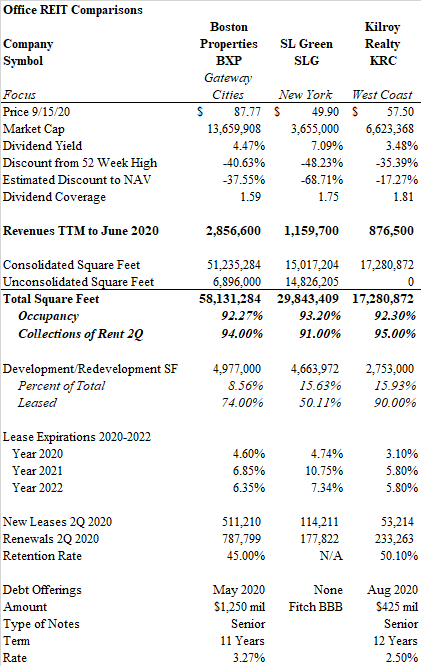

Commercial real estate is under pressure. Hospitality properties are in distress and many retail assets are struggling amid restaurant closures and the acceleration of online shopping. Thus far, long-term leases and high-quality tenant rosters have spared Class A office properties from pain. Second quarter results for major publicly traded office real estate investment trusts offer insights into the office markets of large cities, and their discounted stock prices appear to be attractive.

The second quarter

results for three office REITs were reviewed for this report: Boston Properties

(BXP), SL Green (SLG), and Kilroy Realty Trust (KRC).

Boston Properties is the

nation’s largest office REIT with over 51 million square feet owned directly,

and another 7 million owned through joint ventures. BXP has concentrations of

properties in New York, Boston, Washington, D.C., Los Angeles and San

Francisco. SL Green owns nearly 30 million square feet in New York City with

roughly half-and-half split between direct ownership and joint ventures. SLG

also holds nearly $1.2 billion of mortgages, mezzanine loans and preferred

equity positions in other New York properties. Kilroy Realty Trust has over 17

million square feet based on the west coast. It has a larger suburban portfolio

than the others, and its stock has performed comparatively well.

All office REIT executives believe their companies are well-prepared to weather the shift towards work-from-home arrangements. They have raised capital at low interest rates and bolstered their balance sheets. Lease expirations are minimal in the near term. Stocks are trading at considerable discounts to underlying asset values and offer hefty dividend yields. The ability to sustain dividend payments for the next two years seems likely and the discount to net asset values offers downside protection. Technology companies continue to lease new space. However, clouds hang on the horizon. A reduction in office floorplans seems inevitable. Financial firms may reduce headcounts as they reckon with tighter interest rate spreads and a rising collection of distressed assets in their portfolios. Meanwhile, working from home may not prove to be the revolution once envisioned in April, but certain jobs will remain permanently remote.

One Vanderbilt, SL Green

Note: This paper contains the opinions and interpretations of the

author. No representations are made regarding the accuracy of the material. The

views do not represent investment recommendations. All readers should perform

their own due diligence before making an investment decision.

Occupancy and Collections of Rent in the Second Quarter

All companies collected over 90% of rents during the second

quarter. BXP suffered from vacancy at its hotel properties, and both BXP and

SLG reported rent collections only slightly better than 50% for their retail

square footage. Yet office rent collections were better than feared. BXP and

KRC collected 98% of office rents and 96% of SLG’s office tenants paid during

the second quarter. Overall occupancy at the end of the June period stood

hovered near 93% for all three firms. However, the actual staff presence in the

buildings was minimal, with only about 10-15% physical occupancy for BXP and

SLG and 25% for KRC estimated during late July.

Financing

BXP and KRC took advantage of the decline in interest rates to

raise significant capital during the past six months while SL Green sold two

assets for over $600 million to bolster the balance sheet. In August, Kilroy

raised $425 million in senior notes at 2.5% due in 2032, and Boston Properties

issued $1.25 billion in senior secured notes at 3.25% maturing in 2031. Kilroy

raised $247 million in a March share offering. No new senior debt was issued at

SLG, although a couple of properties were refinanced. Fitch did affirm a BBB

credit rating for SL Green but revised its outlook to “negative”.

Office REITs trade at significan discounts to their pre-Covid highs.

Shareholder Benefits

All CEO’s believe that their balance sheets are well-positioned

for the next two years. Kilroy increased its dividend by 3% in August and SL

Green purchased $163 million of stock during the second quarter.

Leasing Activity

Despite the pandemic, leasing activity did continue at muted

levels. All three companies renewed about 1.5% of their portfolio with an

approximate retention rate of 50%. BXP signed a major new lease for 400,000

square feet with Microsoft at its Reston, Virginia property. BXP and KRC have

minimal lease expirations over the next three years with KRC at roughly 4% per

year through 2022 and BXP closer to 6%. Kilroy has 85% of its space

concentrated in low and mid-rise buildings. SL Green has minimal exposure in 2020

but faces a worrying 11% expiration level in 2021.

Kilroy and Boston Properties are bullish on markets where

technology and life science businesses are showing resilience and even growth

during the pandemic. While Facebook, Google and Amazon grab the most headlines,

the emergence of laboratory needs in the biotechnology and pharmaceutical

industry is equally fascinating. These companies are viewed as more likely to

take up new space in coming years as the office environment remains necessary

to foster collaboration and company culture. Both firms show interest in the

Seattle market while BXP seeks further growth in the technology hotspots near

the Los Angeles beaches. A notable bright spot during the doom and gloom of New

York City’s pandemic challenges was Vornado’s signing of Facebook to a 730,000

square foot lease in the former post office building near Penn Station.

DropBox headquarters in Mission Bay, San Francisco

Development Activity

All three REITs have significant development activity which

accounts for between 9-15% of the total square footage inventory for each

company. While these developments pose risk should they fall short of targets,

all CEOs noted that they had adequate liquidity to finish the projects. 90% of

KRC’s pipeline is leased while BXP has 74% leased in their upcoming projects.

SL Green has higher leasing risk, as was cited in the Fitch ratings downgrade,

with 50% of new square feet committed. Among all three companies’ projects in

development, the most prominent is the 77 story SL Green tower known as One

Vanderbilt – a 1.5 million square foot building near Grand Central Station

which is 70% leased and opens this week. The project is a landmark $3 billion

asset. The opening generated enough excitement to propel the stock upwards by

over 10%. SL Green is also partnering with a Korean pension fund on the $2.3

billion redevelopment of One Madison Avenue. The space is not scheduled for

delivery until 2024. Kilroy is in a strong position with its development

projects. KRC will soon be opening a 355,000 square foot building in Hollywood

fully leased to Netflix and another 635,000 square foot building in Seattle

100% leased to a Fortune 50 company. Another 285,000 square feet in San Diego

will come online in 2021 with 91% of the space leased.

Sublease Risks

One of the factors most likely to suppress future rents is the

likelihood that surplus space is placed on the market by current tenants. These

subleases become phantom vacancy that is nearly always offered at below-market

rents. CEO John Kilroy did not view the subleasing environment as overly

worrying. In reference to San Francisco in particular, he offered, “Sublease

space in the market right now is about 5 million square feet… 2.3 million was

added during Covid… to put that into perspective, the direct vacancy rate in

San Francisco right now is about 5.4% and sublease is 2.5% of that. To compare

that to the dot-com bust, direct vacancy was 8.3% and sublease space with

6.8%.” However, despite the CEO’s comments, Kilroy identified sublease space in

its 10-Q, the first time in several quarters such information was broken out.

849,000 square feet in the portfolio was listed for sublease, or nearly six

percent of the portfolio. About half the space was noted as vacant. In late

July, DropBox announced it would list 270,000 sf for lease, nearly 1/3rd of its

offices, in the newly opened Kilroy development in Mission Bay, San Francisco.

Meanwhile, Boston Properties was impacted by the bankruptcy of Ann Taylor’s

parent company which occupies 340,000 sf in Times Square. It would seem likely

that even if a bankruptcy restructuring is successful, surplus space will find

it’s way onto the market.

SL Green Challenges

SL Green is the most difficult office REIT to analyze. Nearly half

of the company’s square footage is held in joint ventures which are not

consolidated in the operating revenues and expenses. The company also has a

complicated portfolio of first mortgages, mezzanine loans and preferred equity

positions in various properties in New York. SLG also owns many properties

encumbered by ground leases.

Indeed, some mezzanine loan positions appear to be under pressure.

On September 2nd, it was reported that SL Green bought the $90 million first

mortgage for 590 Fifth Avenue after Thor Equities defaulted on a $25 million

mezzanine note. The property is a 19 story 100,000 sf building. The mezzanine business

cuts both ways for SL Green. A distressed developer who falls behind on their

mezzanine financing could present an opportunity for SL Green to pick up assets

for the value of the first mortgage. In most cases, these will be bargain

acquisitions. Unfortunately, the impairment of a mezzanine loan is in itself a

damaging blow to the balance sheet and the need to muster capital to protect a

junior debt position could require deeper pockets than the company anticipates.

While two asset sales reinforced cash positions, the failed $815

million sale of the Daily News Building in March offered an indication of the

challenges valuing New York office assets in a post-pandemic world after

Deutsche Bank pulled financing for the deal. SLG was able to refinance the

property in June with a $510 million mortgage from a lender consortium. SL

Green is also considering the sale of its two multifamily properties.

Kilroy’s Netflix campus: Academy on Vine

Investment Evaluation

SL Green has seen its stock hammered by the pandemic. Down by

nearly 50%, SLG’s dividend yield exceeds 7%. Boston Properties has faced a 40%

decline and offers a yield of 4.4%. Meanwhile, Kilroy lost 35% since its

pre-Covid highs and yields 3.45%

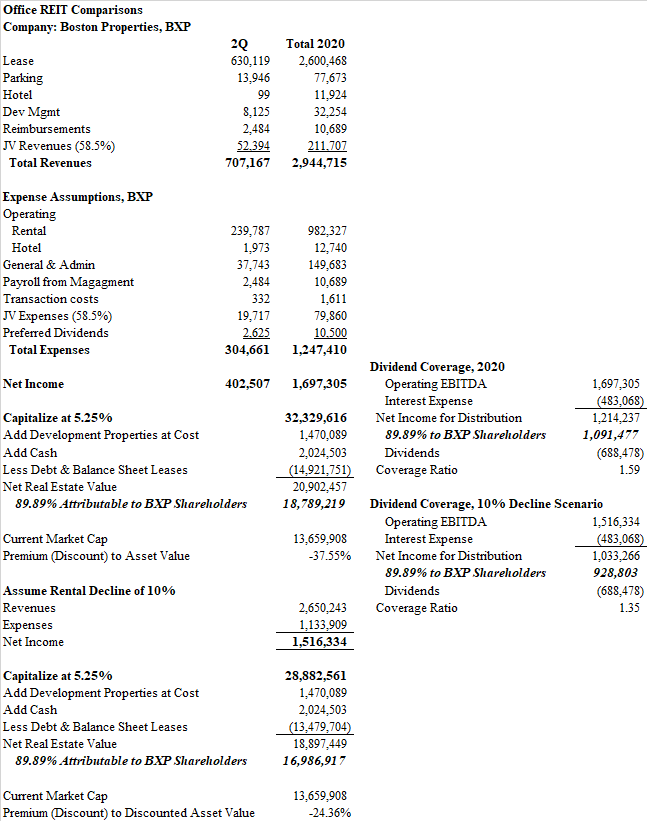

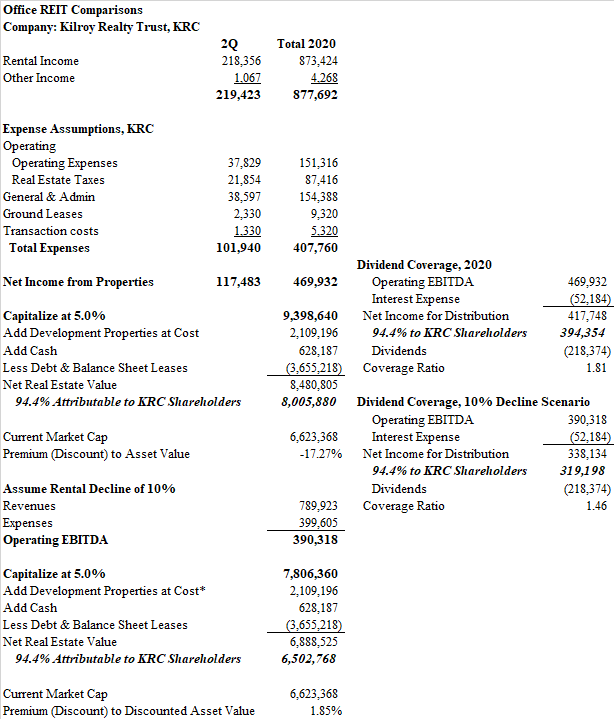

In the process of evaluating the stocks, I made simple

assumptions. Some may argue that these are too elementary, but the exercise was

intended to discover whether the public market is significantly undervaluing

the underlying assets by a wide enough margin to provide an element of downside

protection. I was not intent on arriving at a precise valuation of the

businesses.

My method was to annualize pro forma income simply by taking

second quarter revenues and multiplying them by four. This may prove generous

in the event further occupancy problems arise; it also is punitive for the

companies. For example, the methodology assigns no future income for the

Mission Bay/DropBox property placed in service. It also ignores the 70%

occupancy of One Vanderbilt placed in service by SLG. It gives no value to the

new BXP leasing in Virginia. In all cases, the exercise merely values the development

assets at cost. The only upside “help” that was given by the author was a

slight uptick in hotel revenues attributed to BXP during the balance of two

quarters.

I capitalized the net income at 5.0% for KRC due to its high level

of low and mid-rise buildings, 5.25% for BXP, and 5.5% for SLG. Certainly,

before the pandemic, these cap rates would be considered high for trophy office

properties in major urban areas. I added the cash on the balance sheet and

subtracted debt to arrive at a net asset value. All in-progress development

projects were added at cost. Joint venture assets were included in the income

statement computations to the extent that they were reflected in the ownership

percentages. The result is a 70% value discount for SLG, and a 38% discount for

BXP. KRC is selling for a 17% discount. On the income side, I calculated the

dividend coverage ratios: BXP stands at 1.6x, SLG 1.7x and KRC 1.8x.

Next, I performed a stress test analysis that reduced revenues by

10%. In the case of SL Green, I also deemed their property loan portfolio to be

50% impaired. Even with this penalty, SLG appears to trade at par to net asset

value. Meanwhile BXP would seem to be 24% below value as well. KRC with its

under-estimated future income looks to be valued at par after the stress

test. In this example, BXP and KRC could continue to comfortably fund

their dividends but SLG would be under pressure to reduce shareholder payments.

Paradigm Shift

While all three companies trade at steep discounts, one can’t help

but wonder if the world will look back at this moment and ask why real estate

experts underestimated the paradigm shift of working from home. If it worked

pretty well for 6 months for most office workers, why can’t it work

permanently? If nothing more, workers got 1-2 hours of their days back by not

facing a long commute into the city center. This increase in productivity alone

is tangible.

Of course, as the weeks have dragged on, frustration has set in

with the arrangement. JP Morgan CEO Jamie Dimon has summoned traders back to

their desks and recently noted a decline in productivity among employees at the

banking giant. Zoom meetings can’t replace the 80% of communication that occurs

through body language, and even a micro-second lag on a call is maddening after

the third time someone interrupts. The office is a vital asset in our knowledge

and information-based economy. Ideas and culture are the engines of growth. But

data entry, call centers, accounting and routine back office functions seem to

need nothing more than a good workstation in the den along with a high-speed

data connection. Office leases will take 2-5 years to expire, but what if all

companies simply reduced their footprints by 10%? My stress test may prove to

be too light.

Conclusion

Kilroy and Boston Properties are the most appealing investments.

The balance sheets have been fortified and leasing activity for the companies’

new developments is robust. Kilroy’s exposure to suburban markets offers a

hedge against central business districts in major cities, and BXP has a

well-diversified geographic portfolio. Meanwhile, despite the steep discount,

SL Green appears to be the riskiest of the three REITs. The concentration in

New York City is worrisome. While some may argue that the risk is reflected in

the added discount, it is worth noting the SL Green executives had been

appealing to investors as recently as the fall of 2019 that the stock traded at

an unjustified discount of 25% to its peers. A risky mezzanine portfolio and the

complexity of its joint venture arrangements could pose future challenges.

The most encouraging future for office properties lies in the

technology and life sciences industries. Despite recent sublease announcements,

Both Kilroy and Boston Properties are aggressively pursuing these vanguard

companies with visible degrees of success. Meanwhile, the transformation of New

York City into a technology hub is well under way. The question is now raised:

can technology employment grow fast enough to replace the shrinking office

needs of remote workers?

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2020-09-16 01:30:562020-09-16 01:34:05Office REITs: Value Opportunity or Value Trap?