Way of Wade

The alcoholic beverage industry has been experiencing a secular decline since the pandemic boom. So, borrowing an expression from the Hormuz-constrained oil industry, are we nearing tank bottom? Molson Coors, the brewing giant formed through a 2005 merger, looks like a bargain by most standard metrics.

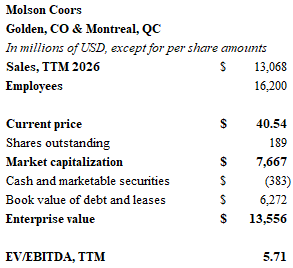

Molson Coors had sales of $13 billion in 2025, representing a 5% annual decline. First quarter revenues ticked up slightly, and management expects 2026 to be a year of stability. The company trades for an EBITDA multiple of 5.7x. The 4.6% dividend yield is well-covered. Cash flow from operations was $1.8 billion dollars in 2025, so there was plenty left over for share buybacks and debt reductions after paying capital expenditures of $700 million and dividends of $376 million.

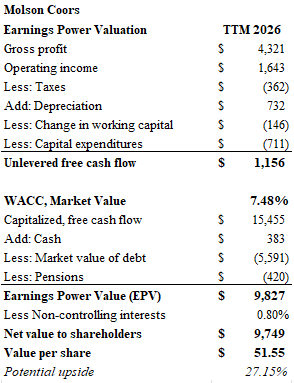

As usual, I calculated the intrinsic value of the business using the earnings power value (EPV) method favored by Bruce Greenwald and his value investment acolytes. This math simply takes normalized unlevered free cash flow and divides it by a weighted average cost of capital to arrive at a gross value for the business. Adjustments are made for cash and debt on the balance sheet to arrive at a net value, or “intrinsic value”.

My intrinsic value calculation shows that the shares trade for a 21% discount. Over the trailing twelve months, unlevered free cash flow amounted to approximately $1.15 billion dollars. I applied a discount rate, or weighted average cost of capital (WACC), of 7.5%. This percentage reflects an equity cost of 9.9% and an after-tax debt cost of 4.1% with a weight of 42%. The resulting quotient is $15.5 billion of capitalized value. Adding cash and subtracting debt and pensions of $6 billion leaves a value of $9.8 billion, or $51.55 per share.

I added some shares of Molson Coors to an account focused on generating income because I think the dividend is well-protected. The yield is better than Treasuries, and much of the downside is priced in. However, I am reluctant to take a large swig at the TAP. The return on capital in 2025 was only about 6.7%. This is less than the WACC of 7.5%. Molson Coors booked $3.6 billion of impairments in 2025, and I suspect more could be in the offing as management seeks to rationalize production. Also, to state the obvious problem, there is no foreseeable sign of growth in the alcohol industry. Finally, margins will continue to come under pressure from high aluminum costs.

Where’s the upside going to come from? Continued share buybacks is one answer. A takeover seems less likely since most brewers are struggling with their own debt hangovers. A leveraged buyout led by the Molson family is my other idea. But why add more debt? This one is for the patient coupon-clippers.

I had much more fun researching Li-Ning, the Chinese athletic footwear and apparel maker. Shares of the company appear to offer an exceptional bargain. And while sales growth is in the low single digits, sales are growing. A lot of the coverage of Nike $NKE and Lululemon $LULU has focused on various management missteps. I suspect one underreported factor has been the role of Chinese competition. The stature of Chinese athletic brands has been rising, and nowhere is this more apparent than on the feet on some of the NBA’s most talented players.

While Nike continues to dominate the NBA shoe league table with the Kobe Bryant, Michael Jordan and Kevin Durant franchises. Chinese brands have made significant inroads. Anta Sports $ANPDY is the largest Chinese brand (another undervalued stock, in my opinion), and has just signed Kyrie Irving to a major deal. 361° features two-time MVP Nicola Jokic. Meanwhile Peak and Rigorer have also made inroads. But the largest deal was recently made by Li-Ning who signed Steph Curry to a $400 million 10-year deal. Curry joins a stable of stars led by Dwayne Wade. The former Miami Heat legend teamed up with Li-Ning several years ago. The Way of Wade line from Li-Ning garners rave reviews from fans, athletes, and “sneakerheads”.

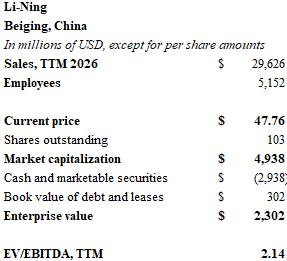

Li-Ning trades in Hong Kong and over the counter with the symbol $LNNGY. At the recent price of $48, the market cap is just below $5 billion. The company has virtually no debt and approximately $300 million of lease obligations. Cash on the balance sheet is an astounding $2.9 billion. They can afford Steph’s contract. With 2025 sales of $4.3 billion and EBITDA of $825 million, the EV/EBITDA multiple is only slightly above 2x. The chart isn’t pretty. The hype from the pandemic spending boom has evaporated, and shares are down over 80% from their peak.

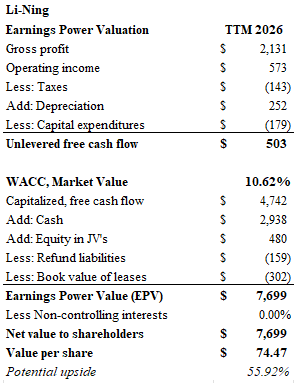

I think Li-Ning shares trade at a substantial 50% discount. Using a weighted average cost of capital of 10.6% and unlevered free cash flow of $500 million, the capitalized value is roughly $4.8 billion. Adding the $2.9 billion of cash and the company’s JV investments while subtracting those leases and about $160 million of warranty liabilities leaves an earnings power value of $7.7 billion or $74.50 per share. It appears that Li-Ning has 56% of potential upside.

The competitive landscape of athletic wear is challenging, to say the least. Hoka $DECK and On Running $ONON are brands that didn’t even register a pulse a decade ago, now they are staples. Meanwhile, spending on athletic apparel could come under pressure as European and American consumers grapple with higher energy costs. Chinese consumers are in year five of a major retrenchment due to the collapse of housing prices. Despite these headwinds, Li-Ning represents an exceptional opportunity at the current market price.

Until next time.

DISCLAIMERThe information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.